The Fed Cuts Rates

Powell’s Capitulation and the Road Back to Money Printing

A couple of days ago, I wrote to you that the Fed’s rate cut was already baked in the cake. And sure enough, yesterday they cut interest rates by 25 basis points, lowering the target range to 4.00–4.25%.

On the surface, that wasn’t a surprise. But after months of Fed Chair Jerome Powell insisting the Fed would stay the course — warning about sticky inflation, and trying to project independence — this sure looked like capitulation to President Trump.

If you’ve been following along, you know Trump’s been on Powell about cuts since before he even set foot back in the Oval Office. And earlier this month, I showed you how he went beyond words and started reshaping the Fed itself — first by installing Stephen Miran, the architect of Trump’s Reset, then by trying to boot Governor Lisa Cook on mortgage fraud claims.

Now, Powell will never admit it — but yesterday’s cut says it all. Trump is winning.

Of course, the Fed dressed it up differently. Here’s what Powell said when pressed about cutting rates without inflation anywhere near their 2% target:

I would look at it this way. We fully understand and appreciate that we need to remain fully committed to restoring 2% inflation on a sustained basis and we will do that. At the same time, we've got to weigh the risks to the two goals and I would say since really since April to me the risks of higher and more persistent inflation have probably become a little less and that's partly because the labor market has softened, GDP growth has slowed. And so I would just say that the risks there have been less than than one might think. And in terms of the labor market, what we're seeing is unemployment is still low. It's still a relatively low rate, but we're seeing downside risks.

Translation: We're cutting rates because we're scared of recession (not because we've “conquered inflation”).

I mean, sure — if you’ve got to do the president’s bidding, then at least try to save face by hinting that not everything is perfect under Trump. That part makes sense.

The problem is that the Fed’s own projections cut straight against this rhetoric.

According to their latest Summary of Economic Projections, they expect GDP growth of 1.6% this year—up from 1.4% projected in June. So, at least on paper, the economy looks better than expected.

What about inflation? Surely, by now they’d at least be projecting it to glide back toward their 2% target before long.

Not really.

Back in June, their projection called for PCE inflation — the Fed’s preferred gauge — to end the year at 3.0%. And yesterday? Still 3.0%. In other words, they’re literally expecting inflation to accelerate from the current 2.6% level, which is already well above their 2% target.

Core PCE — which the Fed also loves to highlight, probably because it excludes such “non-essentials” as food and energy — tells the same story. It’s sitting at 2.9% now and projected to hit 3.1% by year-end, unchanged from June’s forecast.

So let me get this straight: The economy is growing faster than expected, inflation is running hot and expected to get worse, yet they're cutting rates anyway.

Yeah, that sure looks like giving in to Trump.

And don’t forget the market. The S&P 500, Dow, and Nasdaq are all sitting at or near all-time highs. When Powell was pressed on the risks of cutting in that environment — basically, whether he was fueling a bubble — here’s what he said:

You know, we're tightly focused on our goals, right? And our goals are maximum employment and price stability. And so we take the actions that we take with an eye on those goals separately. And that's why we did what we did today. Separately, we monitor financial stability very very carefully. … We don't have a view that there's a right or wrong level of asset prices for any particular financial asset, but we monitor the whole picture really looking for structural vulnerabilities and I would say those are not elevated right now.

That’s just a long way of saying: we’re cornered.

Powell can pretend all he wants that he doesn’t care where the stock market goes. But you know who does care? The White House — especially with the 2026 midterms coming up.

Chalk up another point for Team Trump.

Bottom line: Powell knows inflation isn’t tamed. He knows the market’s frothy. He knows cutting now risks fueling bubbles. But with Trump breathing down his neck, he’s out of options.

Why QE Is Also Already Baked In

It’s no mystery why Team Trump wants lower rates.

The federal government is hemorrhaging cash just to service its gargantuan $37 trillion debt — $1.2 trillion this fiscal year on interest alone. That’s more than the entire U.S. military budget.

Cheaper rates could take some of the sting out of that bill.

Of course, some pesky naysayers like me might point out that the real solution would be to cut spending, bring the budget closer to balance, and actually reduce America’s debt-to-GDP ratio. But let’s be honest — that’s just not how Washington operates, no matter which party happens to be in charge.

That aside, Trump also likes lower rates because they juice the economy — higher wages, soaring stock prices, cheaper mortgages, and a short-term boom that looks and feels like prosperity.

And so here we are: the Fed is cutting. And the projections say they’ll keep cutting. There are only two meetings left this year — October and December. Back in June, the forecast suggested one more cut. Now it shows two. The market agrees: before the meeting, odds of two cuts were around 60%; after, they shot up near 80%.

Another victory for Trump.

But here’s the problem.

The Fed only controls short-term rates. Long-term rates — like 10-year Treasurys and mortgages — are set by the market.

In other words, the Fed can’t just wave a magic wand at an FOMC meeting and force interest rates lower across the entire yield curve. Case in point: between September and December 2024, the Fed cut rates three times by a full percentage point — yet U.S. government bond yields actually went up by 1%.

And that means one thing: the Fed will have to dust off quantitative easing (QE) and directly intervene in the bond market.

You’ve probably heard of QE — it’s when the Fed buys government debt, creating artificial demand for Treasurys to push yields down. In plain English: money printing that props up Wall Street while sticking Main Street with the bill.

QE is, of course, the opposite of QT (quantitative tightening), where the Fed sells off securities or lets them mature in an attempt to pull money out of the system and tame inflation — something the Fed has supposedly been doing since 2022.

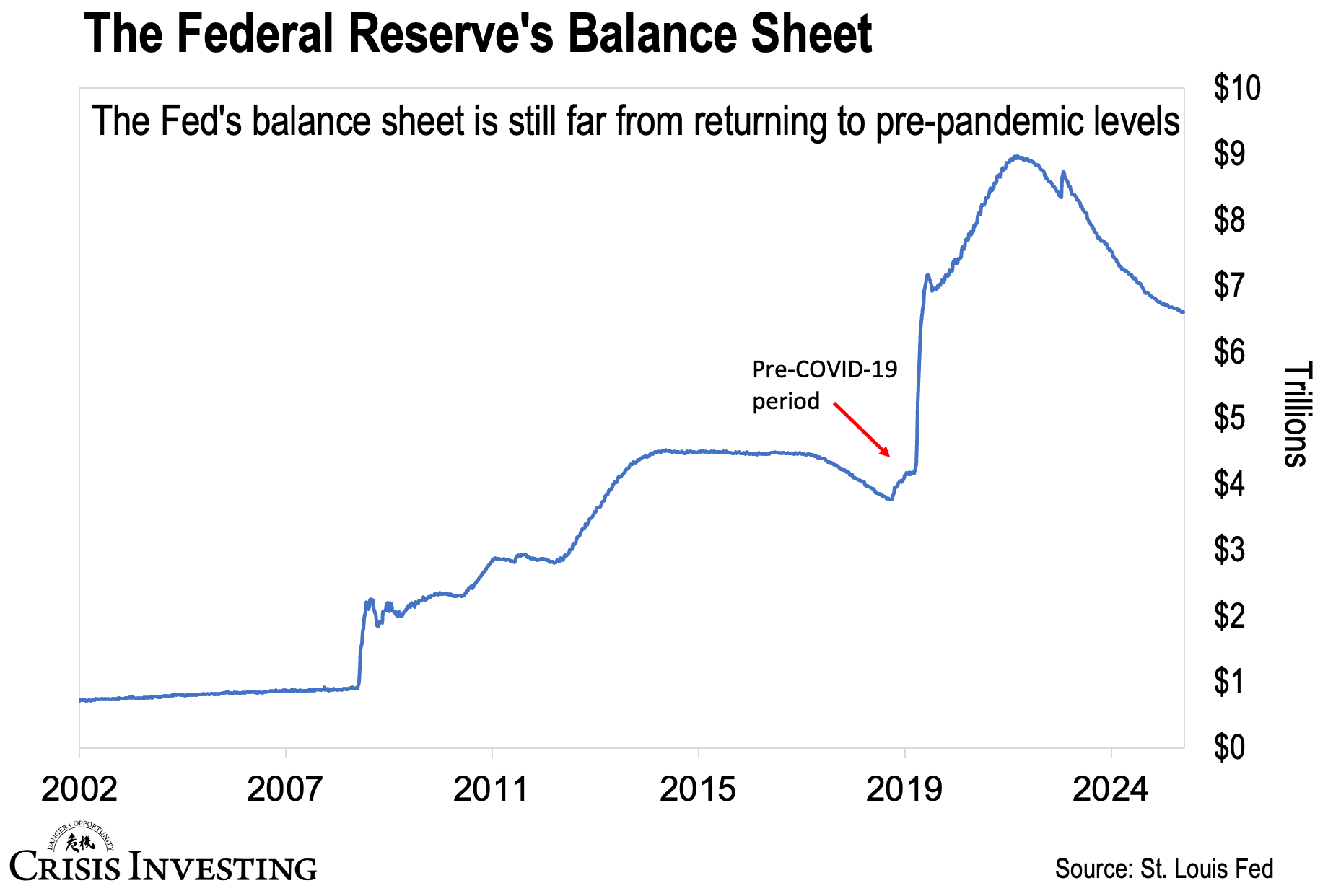

Trouble is, their so-called QT program has been pathetically ineffective. Take a look at the next chart.

After three years of "tightening," the Fed's balance sheet sits at $6.6 trillion—down just 27% from the pandemic peak of $9 trillion. They're nowhere close to pre-pandemic levels of roughly $4 trillion.

Which means that when the Fed inevitably restarts QE to push long-term rates down, it’ll be starting from an already bloated balance sheet.

And that’s the problem.

Remember what happened when they conjured $5 trillion out of thin air during the pandemic? Inflation ripped to 9% — the highest in forty years.

Kicking off the next money-printing cycle from $6.6 trillion instead of $4 trillion — with so much pandemic-era cash still sloshing around the system — all but guarantees double-digit inflation. We’re talking about potential currency destruction on a scale — and at a speed — America has never seen.

Position accordingly.

Regards,

Lau Vegys

P.S. We believe the Fed’s move back into easy money will set off a massive bubble in commodities — especially in monetary metals like gold and silver. That’s why a big portion of our Crisis Investing portfolio is in mining stocks, which Doug Casey himself owns. Now, you might think you’ve missed the boat with gold at record highs and silver at 14-year highs. But as I pointed out earlier this week, mining stocks are still sitting near their cheapest levels in relative terms. Be sure to check out that essay if you missed it.

To be fair, the Fed's choice is:

1- Damned if you do.

2- Damned if you don't.

Their "dual mandates" oppose each other and the government has not cooperated at all by cutting any significant spending.

I will say it would be better to keep rates where they are, preserving the value of the currency and be villified as Paul Volker was during "his recession". That takes having a spine with thick skin.

END THE DAMNED FED. NOW. RIGHT NOW!