Dear Crisis Investing Subscribers,

How serious is this dust-up with Iran? My opinion is that it’s super serious... likely to spin out of control.

That’s Doug Casey, speaking just days after the U.S. and Israeli strikes on Iran that killed Supreme Leader Ali Khamenei and triggered what’s now shaping into the most significant Middle East conflict in decades.

Doug continued:

I thought that both the stock and bond markets have been very overpriced for a long time. I don’t want any part of the general stock market and I think it could crash.

They’re floating on air.

This war could be the catalyst... the pin that the bubble has finally found.

He’s right. And the developments over the past ten days suggest this situation is only getting more serious—not less.

Which is why I’m sending you this alert with a new recommendation—a position designed to capitalize on the crisis unfolding in real time and the market vulnerabilities that will persist long after the headlines fade.

But before we get to that, let me bring you up to speed on the latest developments.

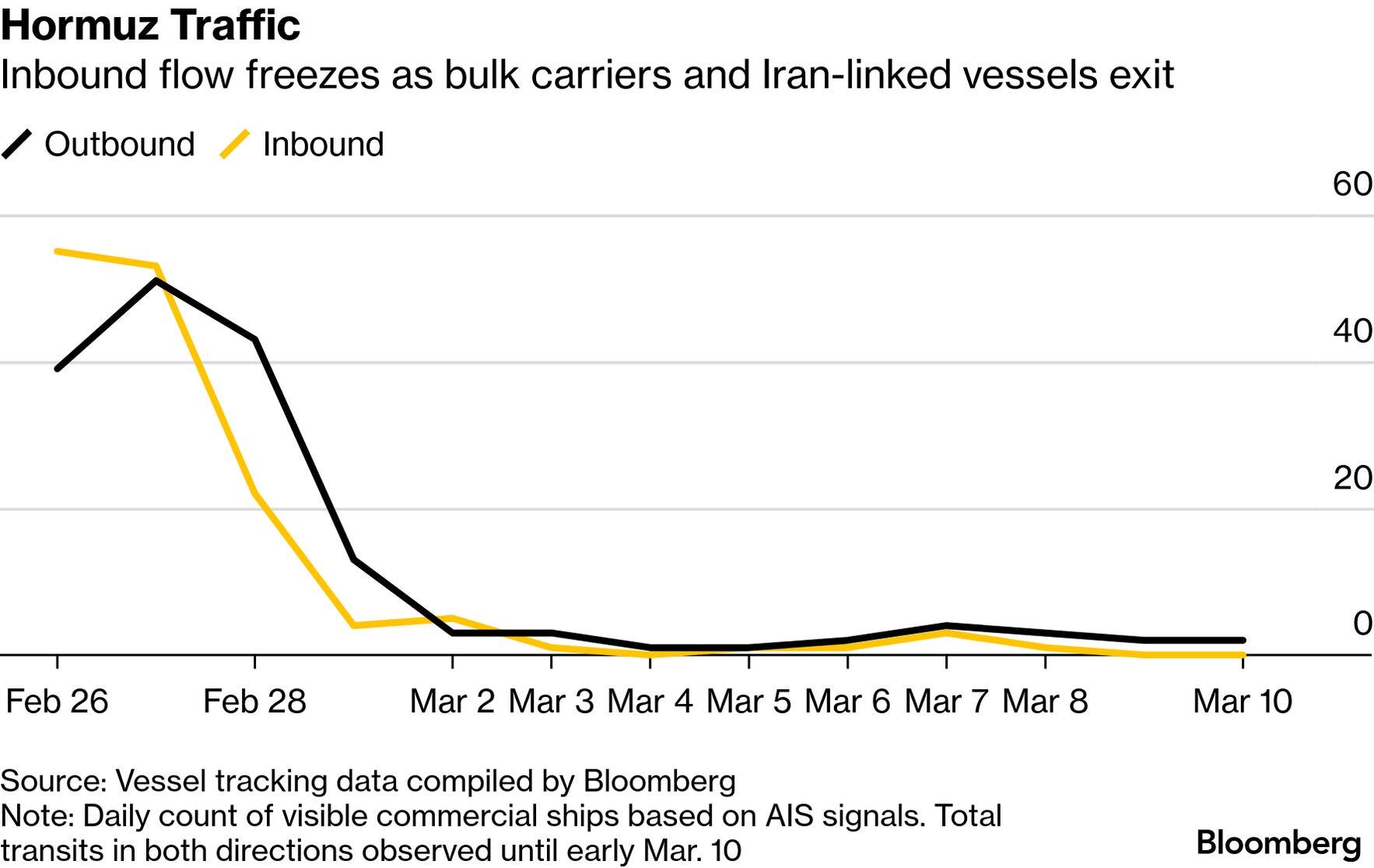

As I wrote to you last week, the Strait of Hormuz—the narrow waterway through which 20% of the world’s oil supply passes—has effectively shut down. Tanker traffic dropped 90% from normal levels by March 4th. On March 2nd, a senior official in Iran’s Islamic Revolutionary Guard Corps (IRGC) officially confirmed the strait was closed and threatened any ship attempting passage.

At least five commercial vessels have been struck by drones or missiles near the strait since the conflict began. Two Indian crew members were killed when the oil tanker Skylight was hit north of Oman. Another vessel was struck by a drone boat, sparking a fire and explosion. A port worker died when the U.S.-flagged Stena Imperative was attacked twice at the port of Bahrain.

In short: the Strait of Hormuz has become a war zone.

As a result, major container shipping companies—Maersk, CMA CGM, Hapag-Lloyd—have suspended transits through the strait entirely. War-risk insurance premiums have spiked from 0.125% to as high as 0.4% of ship value per transit. For very large oil tankers, that’s an increase of roughly a quarter million dollars per passage. Most insurers have simply pulled war-risk coverage altogether.

The U.S. has offered naval escorts. President Trump even demanded in a Truth Social post that tankers “show some guts” and keep moving. But the reality on the ground—or rather, on the water—is that commercial shipping remains at a near-standstill, as you can see from the graph above.

Oil prices have reacted accordingly. WTI crude briefly spiked to nearly $120 per barrel on Monday—the highest since 2022—before pulling back sharply amid talk of strategic reserve releases. As of this writing, it’s trading around $84-90, still well above pre-crisis levels.

Meanwhile, as I wrote in a recent essay, the clock is ticking for Gulf oil producers. When storage capacity runs out, they’ll be forced to shut down wells. Everyone’s in trouble. The UAE has alternative pipelines but they can’t handle full export volumes. Even Saudi Arabia—which has the most storage capacity and the East-West Pipeline to bypass Hormuz—faces a massive hit to export revenues.

Here’s why that matters beyond just oil prices: For decades, Gulf oil producers have been recycling their oil revenues into U.S. financial assets—Treasuries, stocks, corporate bonds, real estate. They’re some of the largest foreign buyers of American assets. Saudi Arabia, the UAE, and Kuwait alone held over $1 trillion in U.S. financial assets as of late 2024. When their oil revenues collapse, their fiscal balances flip from surplus to deficit almost overnight. And when that happens, they don’t just tighten belts domestically—they start pulling capital back. That means selling U.S. Treasuries, liquidating equity positions, repatriating hundreds of billions of dollars. The result? Treasury yields spike. Corporate borrowing costs surge. Stock markets don’t just face selling pressure—they crash. You get the picture.

And this isn't hypothetical. Iraq has already shut down its largest oil fields—production is down 60% as storage tanks hit capacity. Kuwait and the UAE have followed with their own cuts. Qatar stopped LNG production entirely and declared force majeure on gas contracts. The revenue collapse is happening right now.

Meanwhile, against this backdrop, back over at home, the U.S. economy was already showing significant stress before any of this started. Last month saw 92,000 jobs lost—the third time in five months the economy has shed jobs. People are tapping 401(k)s at record rates. Consumer debt sits at all-time highs. I could go on and on.

Yet the stock market—up until very recently—has acted as if none of this matters.

That’s because the market has been floating on something else entirely: artificial intelligence hype and the handful of mega-cap tech stocks riding it.

The top 10 stocks in the S&P 500 now account for roughly 40% of the index’s total weight. At the dot-com peak in 2000, that figure was around 25%. The so-called Magnificent Seven alone contributed roughly 42% of the S&P 500’s total return in 2025.

And those valuations rest entirely on one assumption: that AI spending pays off. Tech giants are projected to spend over $700 billion on AI infrastructure in 2026. The problem? American consumers spend only $12 billion a year on AI services. That’s the gap between vision and reality—between Singapore and Somalia.

We’ve seen this before. In the late 1990s, telecom companies spent hundreds of billions laying fiber optic cable for an internet boom that took years longer to materialize than investors expected. When the revenue didn’t show up on schedule, the entire sector collapsed.

Today’s AI buildout is following the same pattern—except the spending is even larger, and it’s all concentrated in the same handful of stocks propping up the entire index.

It’s an extremely fragile structure.

Add a major geopolitical shock on top of that, and you have a setup where even a modest shift in sentiment could send the whole thing tumbling.

Which brings me to today's recommendation.