The Clock Is Ticking for Gulf Oil Producers—And the Global Economy

Chart of the Week #92

Earlier this week, I wrote about Iran’s closure of the Strait of Hormuz and what it means for global oil markets. Since then, a few things have happened—none of them good.

The insurance market hasn’t budged—and without insurance, no shipping company will risk sending tankers through a war zone, regardless of what governments promise. Trump announced the U.S. would provide naval escorts for tankers and offer political risk insurance through the Development Finance Corporation, a federal agency that provides financing for international projects. But the strait remains effectively closed. Now, it's true that one tanker made it through with its tracking system turned off—but that's hardly a sustainable model for global energy trade. Iraq is already shutting down oil wells because storage is full and tankers can't move.

On the demand side, countries that depend on Gulf oil are scrambling. Pakistan is asking Saudi Arabia to reroute supplies through the Red Sea port of Yanbu. Japanese refineries have requested their government release strategic oil reserves. China halted diesel and gasoline exports to conserve domestic supply. Everyone's trying to avoid running dry.

But the bigger question—the one I raised in Tuesday’s piece—is how long this lasts before producers start shutting down wells. A few days? Painful but survivable. A couple of weeks? Now you're destroying supply. Because once you shut a well, you can't just flip it back on. Permanent production damage starts accumulating—and the longer this drags on, the more of that damage becomes irreversible.

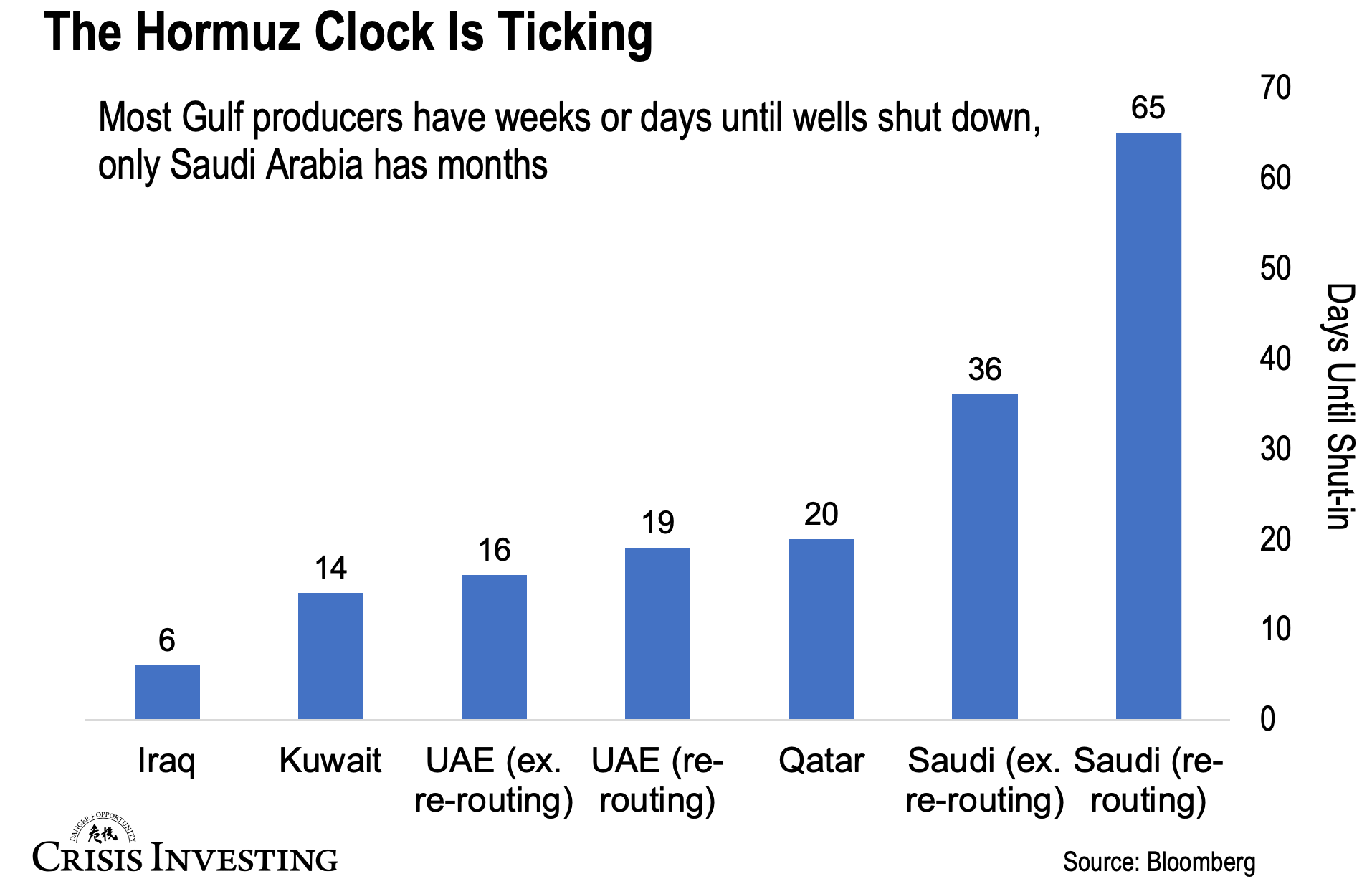

Here’s what that timeline looks like for each country.

Note: The chart shows two scenarios for Saudi Arabia and UAE. “Excluding re-routing” assumes they rely only on Hormuz; “re-routing” shows the extended timeline when using their alternative pipelines—Saudi Arabia’s East-West Pipeline (5M bpd nominal capacity, up to 7M bpd max) and UAE’s Habshan-Fujairah pipeline (1.5M bpd)—which bypass Hormuz through Red Sea ports. However, these pipelines cannot replace full Hormuz export volumes.

Look at the numbers. Iraq has six days. Kuwait has 14. The UAE gets 16 days without rerouting, 19 with it. Qatar has 20. These countries are effectively trapped—even the UAE’s alternative pipeline barely moves the needle. If the strait stays closed, their oil stays in the ground.

Now, Saudi Arabia is different. The Saudis get 65 days if they use their alternative pipeline versus 36 days if they don’t. That’s real runway—but it doesn’t solve the problem.

I say this because even with these alternatives, the volumes don't add up. Combined, those pipelines handle maybe up to 8.5 million barrels per day at maximum capacity. The Strait of Hormuz normally carries over 20 million. So yes, Saudi and the UAE can keep some oil flowing. But they're still taking a massive hit to export revenues.

In short, everyone gets hurt. Some just have more runway.

In case it's not obvious why this should matter to you: when these countries can't export oil, global supply tightens and prices spike. Your gas bill goes up. Shipping costs go up. Everything that needs to be manufactured or transported gets more expensive. It's the kind of inflation shock that can tip economies into recession. The 1970s proved that. And we’re already seeing it—oil’s up about 15% since this started.

But there’s another way this hits American wallets—one that most people aren’t discussing.

It has to do with what Gulf producers do with all those oil dollars.

For decades, Gulf oil producers have been some of the largest buyers of U.S. assets. They sell oil, collect dollars, and recycle those dollars back into U.S. Treasury bonds, U.S. stocks, U.S. real estate. This is the so-called “petrodollar recycling” system, and it’s been a cornerstone of American deficit financing since the 1970s.

We're not talking pocket change here either.

Saudi Arabia, the UAE, and Kuwait held a combined $300+ billion in U.S. Treasury securities as of late 2025. And that’s just Treasuries. When you add corporate stocks and other bonds, these three countries alone held $1.11 trillion in U.S. financial assets as of late 2024. The UAE’s sovereign wealth funds—ADIA, Mubadala, and ADQ—manage around $1.7 trillion in total assets, much of it deployed in U.S. markets.

These are just the three biggest holders. Qatar, Iraq, Oman, and Bahrain hold significant U.S. Treasury and equity positions as well. Their collective participation in U.S. debt and equity markets helps keep borrowing costs low and liquidity high.

Now imagine what happens if their oil revenues collapse.

If these countries can't export, their fiscal balances flip from surplus to deficit almost overnight. Remember, these aren't diversified economies. They produce oil. That's the revenue base. When it disappears, they don't just tighten belts domestically—they pull capital back. That means selling U.S. Treasuries, liquidating equity positions, repatriating hundreds of billions of dollars. Treasury yields spike. Stock markets face selling pressure. Borrowing costs rise for corporations, homebuyers, the federal government. Americans feel it in mortgage rates, car loans, and 401(k) balances.

How long can the strait stay closed before Gulf producers start making hard choices about their foreign holdings? Nobody knows. But the clock is ticking.

Regards,

Lau Vegys

P.S. The kind of geopolitical risk we’re seeing in the Strait of Hormuz is exactly why Doug Casey believes the case for precious metals has never been stronger. In our latest Crisis Investing issue, we feature a fully permitted gold mine on the cusp of restarting production—the kind of developer play that hasn’t been repriced yet despite gold trading above $5,000. We also sit down with Doug to discuss how he’s navigating 2026: metals, energy, geopolitics, and where he sees the biggest opportunities this year.

Another interesting dilemma. Trump offers to turn on the magic money machine (insurance). I’m sure it’s a nice gesture to the owners of the ships and cargo. Not sure it will convince Captains and their Crews however. Rumor has it you can’t simply print them.

All true, and alarming.