The Worst Central Banker in the World

I watched a central banker print my family's savings to zero. Kevin Warsh just inherited the same job.

Let me tell you about the last central banker I grew up under in the Soviet Union.

His name was Viktor Gerashchenko. Soviet banking royalty, in the way only Soviet aristocracies could be — his father ran the financial directorate of the Foreign Ministry, and later served as deputy chairman of Gosbank, the Soviet central bank. The kind of pedigree that put a family one rung below the Politburo.

By 28, the younger Gerashchenko was already running a Soviet bank in London. By the late 1980s, he'd done his father one better — taking the chairman's seat at Gosbank itself. He was at the helm of the Soviet financial system as the whole thing started to come apart.

If you know anything about the Soviet Union in the early 1990s, you probably know about the currency collapse that followed. What you may not know is the central role Gerashchenko played in it. As the system fell apart, he didn’t try to stabilize the ruble — he reached for the printer. Loose monetary policy. Cheap credit to failing state banks. Ruble emission to keep a dying system propped up. Inflation that had been quietly building through the late 1980s exploded into hyperinflation. Prices doubled. Then doubled again. And across the former Soviet sphere, people watched their lifetime savings evaporate in real time.

Families who had spent decades putting money into Soviet ruble savings accounts — for retirement, for apartments, for their children’s future — suddenly discovered those savings were becoming worthless. By the month. Then by the week. Then by the day.

People in my family lost everything. So did most of the people I grew up around. A lifetime of work, gone.

So what did they do? Promote him. In 1992, Gerashchenko was made chairman of the Russian Central Bank — and proceeded to do the same thing, but bigger. The Russian money supply expanded by 18 times in 1992 alone. Yes — eighteen times. In one year.

The disaster culminated on October 11, 1994 — a date now known in Russia as Black Tuesday. The ruble crashed by over 25% against the dollar in a single trading day.

Gerashchenko was fired weeks later. The Harvard economist Jeffrey Sachs called him “the worst central banker in the world.” Quite a distinction in a field where the day job is debasing money.

Powell’s Legacy

I’ve been thinking about Gerashchenko lately because Jerome Powell’s last day as Fed Chair was exactly a week ago.

Let’s take a quick look at his legacy.

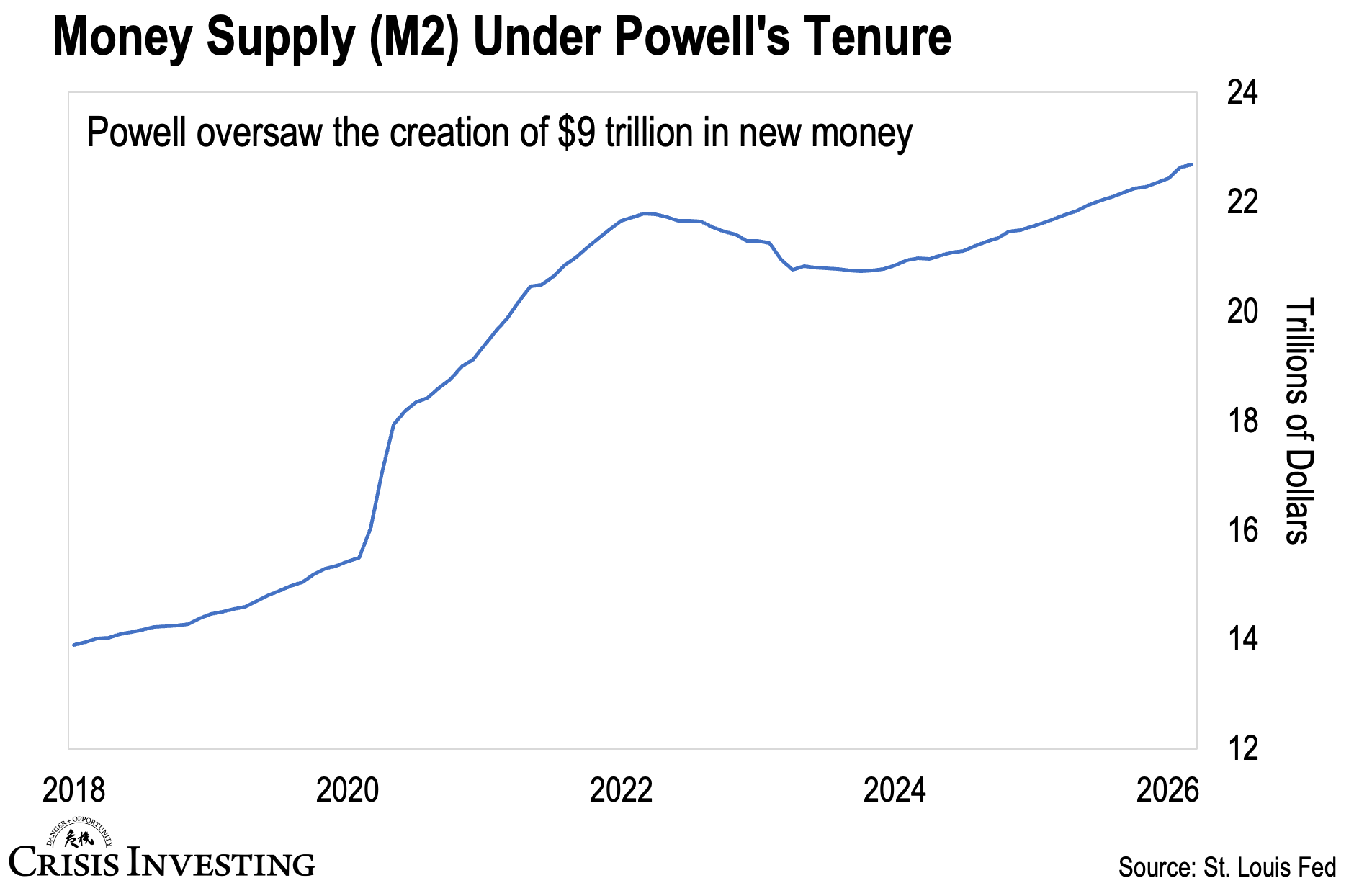

He took the job in February 2018. Eight years in the chair. In that time, the U.S. money supply went from roughly $14 trillion to $22.7 trillion today. That’s $9 trillion in new money created under one man’s watch.

You can see most of it in the chart. That vertical spike in 2020 is the COVID money flood — when the Fed printed roughly $6 trillion in a matter of months. Then came the supposed “tightening.” From mid-2022 onward, the money supply dipped — briefly — before turning back up in late 2023. It never looked back. As of March, we’re at an all-time high.

On the inflation side, the record is just as bad. Persistent inflation above the Fed’s 2% target through most of his tenure. A peak of 9.1% in 2022 — the worst in 40 years. And now re-accelerating again under the Iran war.

What did the Fed do about it? They cut rates. Three times in 2025 alone, while inflation was still running above target. When you cut rates, you make borrowing cheaper, which means more money flowing into the economy — the exact opposite of what you’d do if you were serious about fighting inflation.

And yet Powell is walking out the door to polite applause from the financial press. Nobody is calling him “the worst central banker in the world.” Why not?

Because his timing was impeccable. He’s exiting the stage right before the real consequences land.

Which brings us to his replacement. Trump’s man. Kevin Warsh.

Trump’s Man

The Senate confirmed Warsh two days before Powell stepped down. He got the job for a very specific reason.

As you probably remember, Trump and Powell did not get along. Trump openly called Powell an “idiot,” a “dummy,” an “imbecile” in front of reporters. The complaints came almost weekly. The reason was simple. Trump wanted rate cuts. Trump wanted easier money. Powell wouldn’t deliver — at least not as fast as Trump wanted.

So Trump went looking for someone who would. Warsh has close ties to the Trump family. He’s worth somewhere around $200 million, most of it through his wife — an heiress to the Estée Lauder cosmetics fortune. He’s been quietly waiting for this job for the better part of a decade.

Here’s the irony, though. Warsh was a Fed Governor under Ben Bernanke from 2006 to 2011, where he built his reputation as one of the most hawkish voices on the board. He opposed expansive QE. He resigned, in part, because he disagreed with the Bernanke Fed’s willingness to keep the printer running.

Now he’s been brought back to do exactly what he once opposed.

So what’s the plan?

Officially, the opposite of what Trump wants. In a 2025 Wall Street Journal op-ed, Warsh called the Fed’s balance sheet “bloated” and said the central bank needs to reduce its footprint. He repeated the line in his Senate confirmation hearings just weeks ago. Shrinking, he said, would let the Fed get back to its traditional tool — the policy rate — instead of running monetary policy through balance-sheet operations.

Sounds reasonable. Except it can’t actually be done.

To shrink the balance sheet, the Fed has to either let Treasury securities run off without reinvesting, or sell them back into the market. Either way, somebody else has to buy the bonds the Fed isn’t holding. And the buyers it might find — pension funds, insurance companies, foreign central banks — are already heavily exposed to Treasuries and demanding higher yields to absorb more.

We just saw exactly that play out last week. The 30-year cracked 5% — the highest the long end has been since the run-up to the 2008 financial crisis. The bond market is telling Washington it has no appetite for more debt at lower yields. And every tick higher on the long end costs the U.S. government roughly $390 billion a year in additional interest at current debt levels.

So if Warsh actually tries to shrink the balance sheet, he pushes the long bond even higher. Which makes the federal debt math worse. Which forces the printer back on.

What he says he’ll do, in other words, is exactly the opposite of what the math will let him do.

But here's the part most people are missing: the money printer is already on.

In December 2025 — while inflation was still running well above target — Powell quietly launched a new program. $40 billion a month in Treasury bill purchases. No announced end date. They called it “reserve management.”

It’s stealth money printing. Same plumbing as quantitative easing — the Fed creates reserves out of thin air, uses them to buy Treasury bills, and the money supply grows. The only difference is that it’s targeting short-term bills instead of long-term bonds, which gives the Fed cover to say it’s not stimulus.

And that program is still running. Right now. While inflation re-accelerates under the Iran war. While the bond market is telling the Treasury to pay up.

Warsh isn’t walking into a question of whether to print. The printer is already on. He’s walking into a question of how fast to push it.

What Warsh Is Walking Into

Why can’t Warsh just hold the line? Because the math doesn’t let him.

$39 trillion in federal debt today. $65 trillion projected by 2036 per the government’s own numbers. Interest expense doubling from $1 trillion to over $2 trillion within the decade. Roughly $10 trillion of maturing debt to refinance this year alone — every dollar of it repricing into the highest yields in two decades.

The only path that doesn’t immediately blow up the budget is for the Fed to keep buying. The bond market has already voted. The Treasury has nowhere else to turn.

So Warsh prints. Not maybe. Will.

The problem is, he’s not starting from a clean slate.

As I mentioned, the M2 money supply already sits at $22.7 trillion — $9 trillion higher than when Powell took the chair in 2018. The “tightening” the Fed claimed to have done after 2022 never actually unwound anything meaningful. There’s $9 trillion of new money already sloshing around the system.

And it’s all about to land on the worst possible economy to print into.

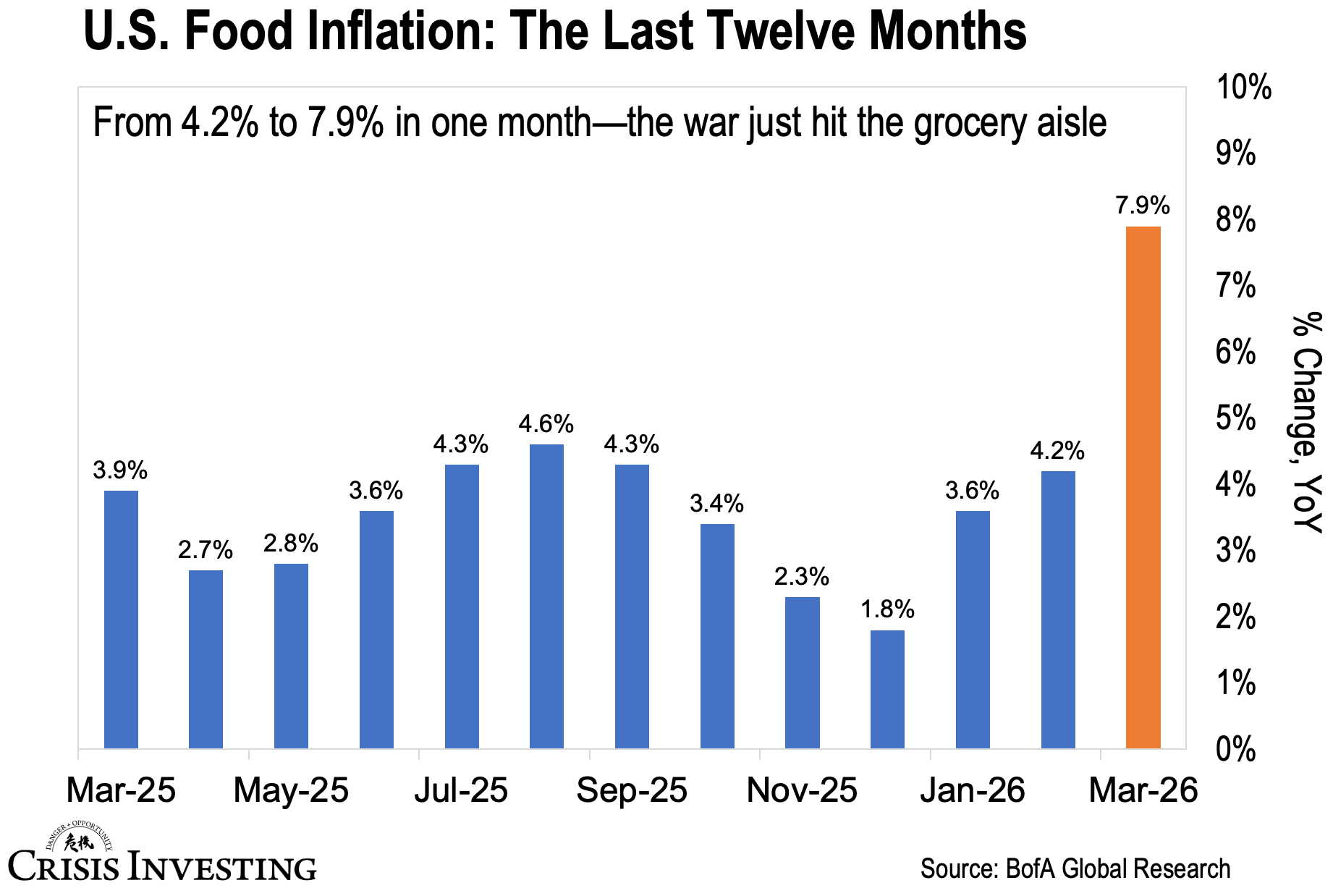

Just look at the latest food inflation print: 7.9% year over year. Tomatoes up 102%. Vegetables up 90%. Beef up over 12%.

A big part of that is the Hormuz crisis. About a third of all seaborne fertilizer trade flows through that same strait. It’s been shut for two months. The price of urea — the main input in nitrogen fertilizer — has more than doubled since February. And that part hasn’t even fully shown up at the checkout yet.

This is what Warsh is walking into.

Print into that, on top of a money supply already at all-time highs, and you don’t get 2020-style asset-bubble inflation. You get the kind of inflation the United States hasn’t seen in fifty years. Maybe much longer.

This is exactly what ended Gerashchenko’s career — a central banker forced to print into an economy that was already broken. The savings of millions wiped out in the process.

As for Warsh himself: Give it a year or two. The man who just replaced Powell is going to wish he never took the job.

Regards,

Lau Vegys

P.S. But where does all this leave you, you might be wondering? Well, let me give you two numbers. Since Trump's inauguration, gold is up about 70%. Silver is up about 150%. And that's with what Trump kept calling an "uncooperative" Fed chair. Under Warsh — brought in specifically to be the cooperative one — I wouldn't be surprised if those numbers double. Maybe triple. That's exactly why a significant portion of our Crisis Investing portfolio is focused on precious metals plays — many of which Doug Casey himself owns.

Massive monetary and fiscal distortions which have been building for 40+ years must be, hence will be, wrung from the system. This can only be accomplished via one of two means; deflationary collapse or inflationary collapse. Given that every currency in the world is fiat inflationary calamity is inevitable. Tangible assets offer refuge, particularly liquid tangibles (i.e. precious metals).

Something about being stuck between a rock and a very hard place.