The Promise of Peace

A good mood, priced on a promise, is an opportunity to build cash.

The hoped for Trump War Put came into play on his birthday and the markets loved it. This next chapter in the peace saga has kept the broad markets buoyant, with but occasional dips. Our long-time happy spaces in gold, silver, uranium and those that dig them out of the ground have begun a recovery as well from what we might choose to call a correction within a longer-term upward trend.

People are believing this current promise of peace, again.

A deal you can’t read and is pointless to critique

We don’t get to see this deal. We’re told it exists. Some bits of it emerge, verbally. I have no ability to influence the deal. I can’t do a damn thing about it. There is nothing solid to critique and neither Trump nor Iran, nor Israel, nor Hezbollah, would waste time reading any suggestions I might make as to what a peace deal should include. So I ain’t gonna bother.

But we can remember that peace still isn’t Trump’s alone to deliver. It takes Iran too, and Iran’s leadership seems pretty messed up right now. Neither party in this deal has earned the confidence and trust of the other. As far as we know, so far, Israel hasn’t signed onto the promised peace deal. Although maybe it has. Who knows. And Hezbollah might lob a wrench into the works, just to keep things burning. And then as far as actually beginning to resolve the war-induced (aka, government-induced) economic distortions caused by the war, there are those pesky insurance underwriters who decide when the Strait of Hormuz actually reopens to Western shipping.

I suggest we treat the market rally as what it is: a mood, priced on a promise, made by people who may or may not be in a position to keep their promises. The broader markets are overvalued by almost every measure, ripe for the next random shot fired in the Middle East or by the Federal Reserve to trigger a decline. Everyone wants the markets to keep shooting the moon, or more apropos this week: shooting for Mars. So it’s reasonable to assume that that hyped up hope will lift the markets for a time. Yay.

This can be an opportunity to create an opportunity.

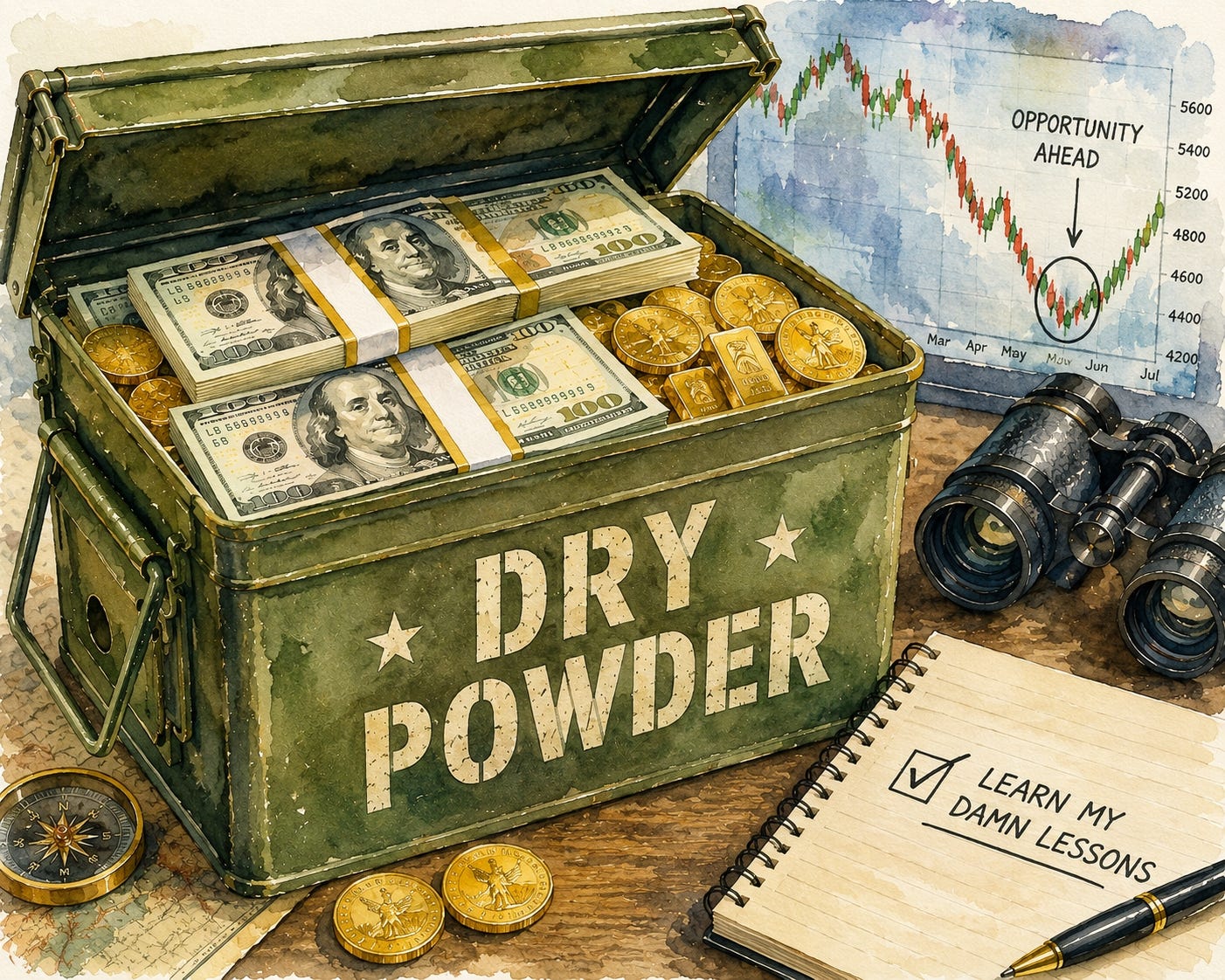

A month ago, and at Matt Smith’s urging, I published an article titled Keep Some Dry Powder, in which I suggested that we all examine our portfolios to confirm we had enough emergency cash, and to build enough dry powder that a major decline would feel like an opportunity instead of a knife in the belly. Soon after, we hit a pretty mean decline of about 20% in the metals and miners.

The current rally in our space is now climbing off these lows. It feels good as our gold, silver and various stocks rise back up. For those of us who need to learn the same lessons over and over in our lives, we’ve had a fresh reminder that in a politically controlled economy, things don’t make sense or follow rules. Whether we like it or not, we need to behave as the speculators that political and central bank shenanigans have incentivized us all to become. I am anticipating that Trump’s Birthday edition of his War Put will give us a chance to build cash positions for those who missed earlier opportunities.

When prices rise on news you can’t verify, sell into the strength as it appears. Best not to wait for the next panic and wish you had.

Over the next days and weeks, look at your winners. Look at the positions you’d be relieved to be out of if the Strait ends up staying shut months more. Trim them if they are in a good-enough price territory and leave that cash in your portfolio. It’s dry powder — an option with no expiration date, the right to buy great assets at panic prices whenever the next panic arrives. And it will arrive.

Keep your survival money walled off and untouched, or start building it if you don’t have any.

Sure, holding cash means you miss some of the upside. But holding no cash means you miss the opportunities the big declines hand you. No cash is high anxiety. No cash is every egg you own riding on market dynamics you don’t control.

Cash is the opposite of all that. Cash is freedom. Freedom to act, freedom to wait. Dry powder isn’t money doing nothing. It’s money ready and raring.

Printing press vs. press release

The Fed Put pays out because the Fed owns the printing press. Trump’s War Put—or I suppose we can call it a Peace Put—pays out only as long as everyone believes it. The first is a perversion with teeth. The second is a wager based on little info and lots of hope.

As for me, I am going to use this evolving rally while the moods run hot. I am going to tap some profits from broader market positions. And as our core metals and mining positions are heading back up, I am going to look to see what I can do without and turn some of it back into cash. It’s all part of playing the long game of speculating in the setting of government actors that will keep causing harm to us all.

Berkshire Hathaway is sitting on a record $397 billion in cash — its highest ever. So it’s not just little old me talking up cash. If one of your friends or family members could benefit from a reminder that hype and hope aren’t plans, that cash is king, that what goes up often comes down, and that anxiety is lower when cash is higher, please forward this email or otherwise share it, so they can read and subscribe to Doug Casey’s Crisis Investing.

Sincerely,

John Hunt, MD

One observation I've made over the years is that many of the investors who have generated truly exceptional long-term returns are value investors. And despite the common criticism of "cash drag," most of them have often held meaningful cash positions, sometimes modest, sometimes very large.

What's interesting is that their long-term outperformance occurred despite carrying this apparent handicap. Cash reduced returns during bull markets, but it also gave them something far more valuable: patience, flexibility, and the ability to act decisively when opportunities appeared.

This is one reason why Berkshire Hathaway's current cash position catches my attention. Not because Buffett is predicting a crash, but because a cash balance of this magnitude, relative to Berkshire's market value, may be telling us something about the availability of attractively priced opportunities.

For value investors, cash is not a failure to invest. It is often evidence of investment discipline.

For mining speculators out there, some of the smaller and mid-tier operators in South America are ripe for future profit creation. Lundin Gold, Aris Mining, Aura Minerals, G Mining Ventures, Lundin Mining, Solaris Resources, Abra Silver, LunR Royalties, Omai Gold Mines, Founders Metals, G2 Goldfields, etc.