Gold Is Down. Here’s Why That’s Actually Good News.

Chart of the Week #95

A few of you have written in this week asking some version of the same question: what’s happening with gold? We have a war in the Middle East, the Strait of Hormuz is closed, oil is through the roof — and gold is going down? What gives?

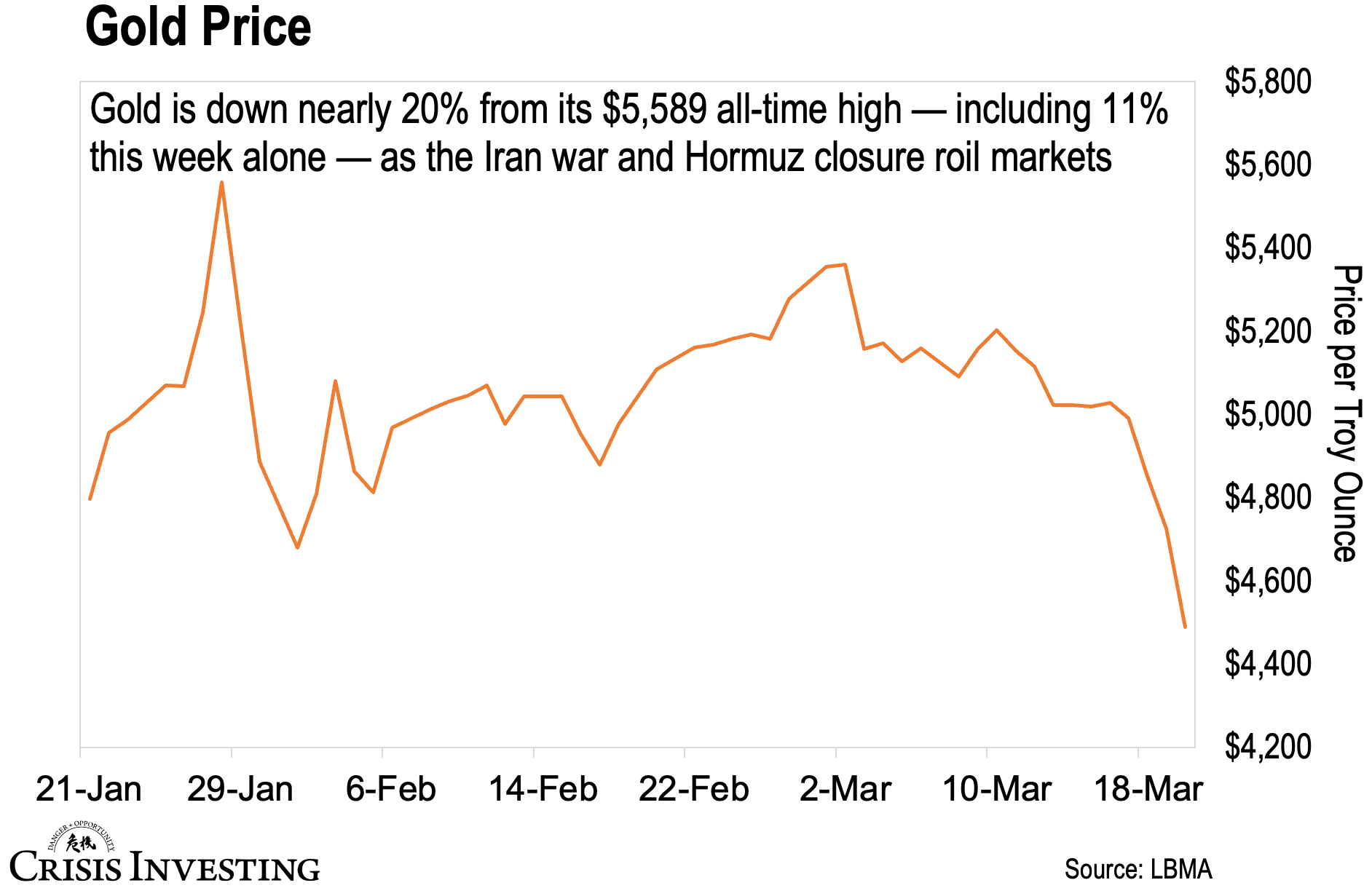

It’s a fair question, especially considering that gold has historically thrived in exactly this kind of environment — uncertainty, war, and inflation. Take a look at today's chart showing gold's price over the past several months — from its all-time high in late January to where it sits today.

Down nearly 20% from its all-time high of $5,589, hit just weeks ago in late January. This week alone it shed 11% — its worst weekly performance since 1983. That’s in the middle of a war that’s shut down the world’s most important oil chokepoint, mind you.

Your instinct is right — this shouldn’t be happening. But here’s what most people are missing: gold isn’t falling because the bull case is broken. It’s falling because of three short-term forces that have nothing to do with the fundamentals. And once you understand what they are, this starts to look a lot less like a reason to panic and a lot more like an opportunity.

Let me quickly run through all three.

The first is the war itself. Once again, geopolitical crises normally send money flooding into safe havens like gold. But this war is stoking inflation. Oil is up more than 40% since February 28th, feeding inflation expectations globally, which in turn has pushed rate cut expectations off the table — for now. And when rate cuts disappear, so does one of gold’s tailwinds — cheaper money and lower real yields.

Then there’s the dollar. It’s been inching up since the war began — not dramatically, but enough to matter. Gold is priced in dollars, so when the dollar strengthens, it gets more expensive for international buyers, and demand softens — or at least the expectation of softer demand takes hold, which is enough to move the price on its own.

The third force — and arguably the most important one — is forced selling. Leveraged funds that bought gold on margin are getting margin calls. They’re selling because they have to. It’s mechanical, indiscriminate, and — most importantly — temporary.

Now, here’s the thing. None of these factors touch the structural case. De-dollarization is still ongoing. U.S. fiscal deficits are still exploding — and will only get worse given the enormous price tag of this war. The stealth money printer is already running. A weak dollar remains the stated objective of the Trump administration. And geopolitical risk is at its highest level in decades. (The rate cut argument, by the way, stops mattering altogether once inflation gets bad enough — because gold doesn’t need cheap money to go up when the money itself is losing value.) The JPMorgans and Deutsche Banks of this world haven’t moved their year-end targets — $6,300 and $6,000 respectively — despite this week’s carnage.

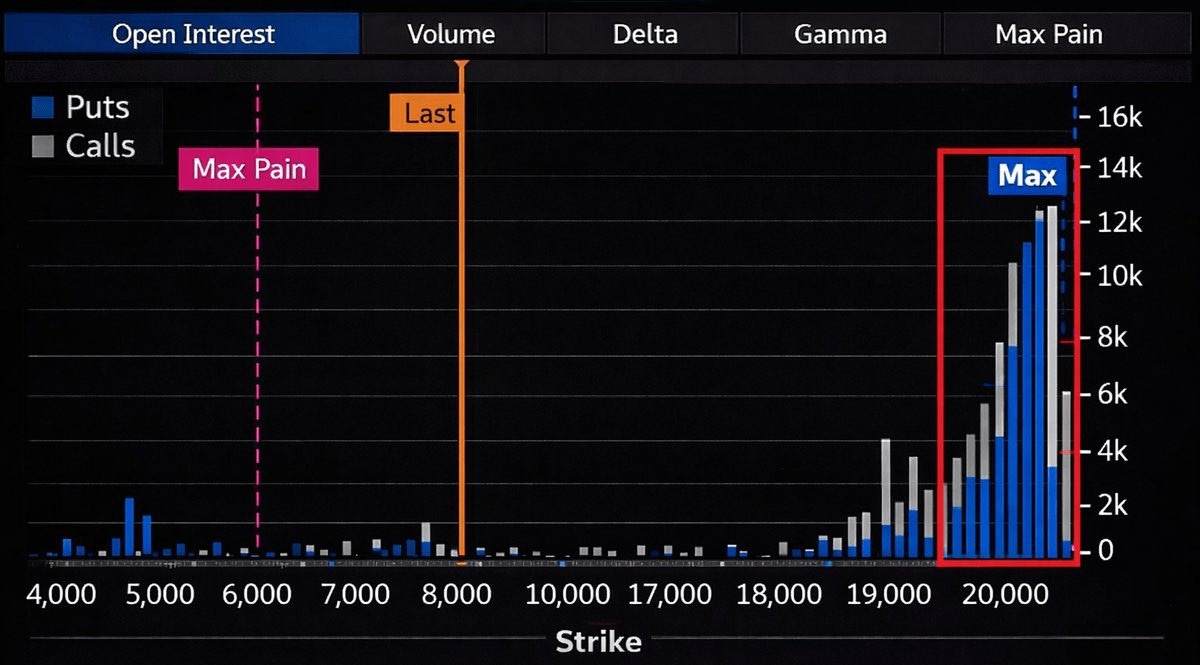

Incidentally, that’s nothing compared to what some people are betting gold could be by year-end. Take a look at this chart showing December 2026 COMEX gold options open interest, broken down by strike price.

As you can see, there's a striking cluster of call positions in the $18,000 to $20,000 strike range. Yes, you read that right. Now, to be fair, these are deep out-of-the-money bets — lottery tickets on extreme upside, not a consensus price target. But the volume is real, and somebody is paying for that optionality. Make of that what you will.

One final point — it’s worth stepping back and looking at what history tells us about oil shocks specifically — because that’s exactly what we’re dealing with right now. During the 1973 Arab oil embargo, oil quadrupled in price almost overnight while gold rose roughly 70% — but not immediately. Much like today, the initial shock created chaos, forced liquidations, and short-term price distortions. In the wake of the 1979 Iranian Revolution, oil surged 110% and gold rose nearly 150% — its biggest two-year gain on record. Both times, the pattern was the same — short-term disruption, then a powerful rally once the monetary consequences of the oil shock worked their way through the system.

Today rhymes. So if you’re open to the very logical possibility that the Iran war — which, from the looks of it, is already becoming a big mess — could unleash the kind of chaos we saw in 1973 and 1979, you probably shouldn’t be selling your gold. In fact, at these prices, you should probably be buying more.

Have a good rest of the weekend,

Lau Vegys

P.S. In our latest Crisis Investing alert, we recommended a position designed to capitalize on the turmoil the Iran war has unleashed. Make sure you haven’t missed it. And even if you’re not a paid subscriber yet, the lead is free to all. On a related note — some of our picks have pulled back alongside gold’s retreat, creating some compelling entry points across the precious metals section of the Crisis Investing portfolio.

I wasn't personally concerned regarding my positioning. But your post is extremely timely and well reasoned. Very much appreciated.

The petrodollar system is on its way out when America can't defend the oil producing monarchies that recycle their dollars into treasuries and the S&P 500.