The Most Important Chemical You've Never Heard Of

Chart of the Week #107

There’s a serious shortage forming in the global market, and it’s centered on an unglamorous chemical 99% of people didn’t even know existed — until the Iran war shut Hormuz. Most still don’t. It’s called sulfur. But it’s used in almost everything. It helps mine and refine your metals. It also helps grow your food. And so much more.

Note: Matt Smith walked through all of this in much greater detail last week. If you haven’t yet read his Shortages Are Coming essay, you probably should.

For decades, sulfur was the cheapest input in the industrial chain — a chemical so abundant that nobody could give it away. You could see it pile up at oil refineries and copper smelters, sold for pennies a pound. As recently as 2024, the average U.S. price was under US$50 a metric ton.

Then came the Iran war, and the Strait of Hormuz shut. As I’m writing this, sulfur is up 95% in three months. Sulfuric acid is up nearly 160% in ten weeks. Bigger moves than oil itself. And almost nobody’s talking about it.

Today’s Chart of the Week tells you why. Take a look.

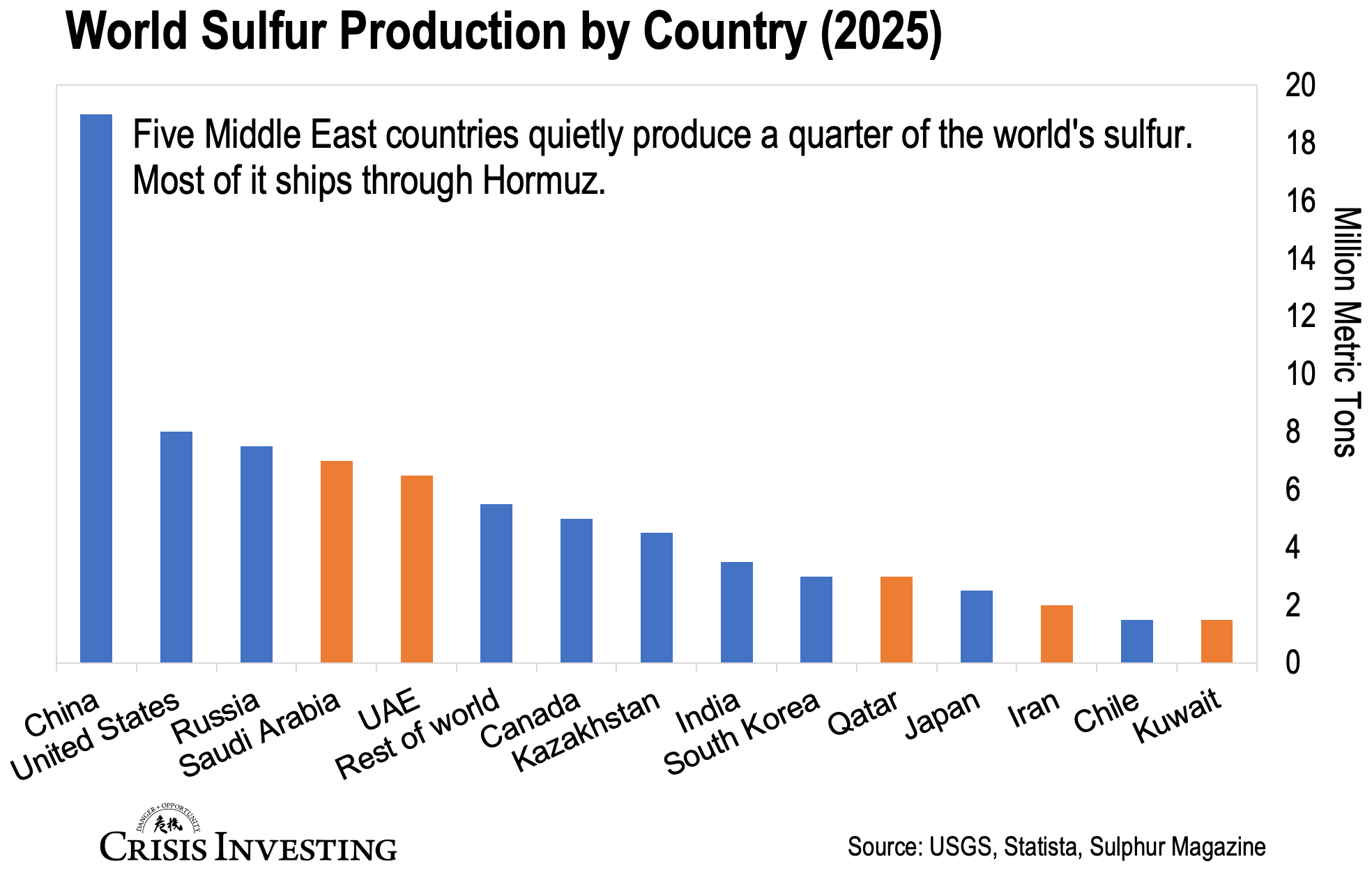

The chart shows you global sulfur production in 2025. The bars that matter — Saudi Arabia, UAE, Qatar, Iran, Kuwait — are highlighted in orange. They’re the Middle East producers, and together they account for roughly 24% of global supply. That’s a big chunk. But consider that these countries move about half of the world’s seaborne sulfur trade through the Strait of Hormuz. That stopped happening about three months ago.

And it probably gets much worse from there.

As Matt stressed in his essay, roughly 60% of the world’s sulfuric acid goes into fertilizer production — specifically phosphate fertilizer, which grows much of the world’s food. The other 40% goes into mining: leaching copper, processing nickel for EV batteries, extracting uranium, refining rare earths.

So when supply collapses, food and metals start fighting over what’s left.

Then there’s the supply side — and it doesn’t flex. Most U.S. sulfur production (~8 million metric tons) and Russia’s (~7.5 million) is locked into domestic value chains — feeding U.S. refiners, U.S. fertilizer plants, Russian metals smelters. Canada and Kazakhstan are also producers, but their volumes feed regional markets. Even India and South Korea, both meaningful producers, have their own domestic acid needs to meet first.

And then there's China — that tallest bar on the chart above. On May 1, the world’s largest sulfuric acid exporter banned its own exports outright — removing roughly 4.5 million tonnes of annual supply from global markets almost overnight.

The damage is already showing up in the numbers. Chile — the world’s largest copper producer — imported 151,000 metric tons of sulfuric acid from China in March 2025. By March 2026, that number was zero. Kazatomprom, which produces 40% of the world’s uranium, has cut its 2026 guidance by 10%, citing sulfuric acid shortages. And in Indonesian nickel — the feedstock for EV batteries — major producer Huayou has idled half its capacity.

We’re putting all of this together in this month’s issue of Crisis Investing, including a recommendation of a company that doesn’t just survive a sulfur shortage — it profits from it.

If you’re a paid subscriber, you’ll have the issue in your inbox in a few days. Keep an eye out.

Regards,

Lau Vegys

technically sulfur is a element , and therefore a chemical. However, it's not a chemical in the same way sulfuric acid is a chemical or other things that we often make with sulfur as an component... or use chemistry to extract sulfur from other compounds such as these hydrocarbon streams. The only reason Sulphur is cheap, besides the fact that it's a great abundance on the Earth, is because we've already got the infrastructure extracting the compounds and we just have to do some final steps of chemistry to get what we need from it. We could do the same thing from mining in other ways. It would just not be nearly as efficient and therefore cost-effective.

... another interesting tidbit that the green movement has no concept of is how much of our comfortable and inexpensive life is provided by hydrocarbon streams.