Shortages Are Coming

The Strait of Hormuz has been closed for 79 days. Most people haven’t noticed. They will.

79 days ago, the Strait of Hormuz closed.

11 million barrels a day stopped moving. The IEA called it the largest supply disruption in the history of the global oil market. Gasoline is $4.53 nationally. Diesel is $5.65. You already know that part.

What you don’t know yet is what comes next.

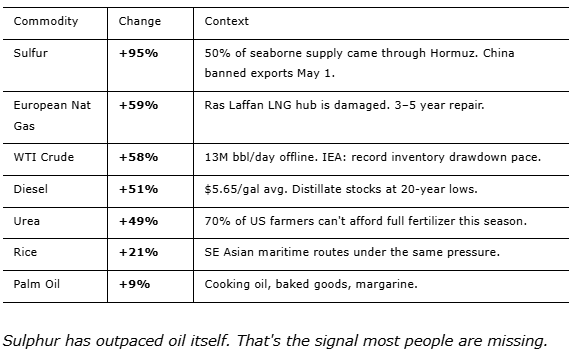

This isn’t an oil story. It’s a cascade. Every refinery that processes crude produces sulphur as a byproduct. That sulphur becomes sulphuric acid. That acid grows your food, mines your copper, and starts your car. The Middle East supplies 24% of global sulphur. Half of seaborne trade moved through Hormuz.

It stopped moving 78 days ago.

The shortages that are coming aren’t priced in.

The Chemical Nobody Is Talking About

Sulphuric acid is the most produced industrial chemical on earth. It’s used in fertilizers, copper mining, semiconductor manufacturing, uranium extraction, lead-acid batteries, EV battery production and so much more.

About 50% of seaborne sulphur trade transited the Strait of Hormuz. In March, global sulphur loadings on dry bulk carriers collapsed 31% in a single month. Persian Gulf exports fell 66%.

Then on May 1, China, the world’s largest sulphuric acid exporter, banned exports entirely to protect its own farmers. Three million annualized tonnes pulled from global markets overnight. Japan, South Korea, and India combined have 500,000 tonnes of spare export capacity. That’s one-sixth of the gap.

The result: sulphuric acid CFR US Gulf went from $155/mt to $400/mt in ten weeks. A 158% increase. Sulphur is up 95% since February 28 — a bigger move than oil itself.

Here’s why that matters for everything downstream.

Metals vs. Food: A War for Acid

Fifty-five to sixty percent of all sulphuric acid goes to fertilizer production. The rest goes to mining: leaching copper, processing nickel, extracting uranium, refining rare earths. When supply collapses, those two sectors fight over what’s left.

Governments will be the ones to decide: Does the remaining supply go to food or to industry? Normally food would be the obvious choice. But, in a time of war will that decision change?

The supply constraints for mining are already showing up in the numbers. Chile, the world’s largest copper producer, imported 151,000 tonnes of sulphuric acid from China in March 2025. February 2026: 32,000 tonnes. March 2026: zero. About 20% of global refined copper production depends on acid-leach operations. That’s a physical availability problem, not a price problem.

Kazatomprom — 40% of global uranium supply — has already cut 2026 guidance by 10% citing sulphuric acid shortages for in-situ recovery. One of their major joint ventures was cut from 6,000 to 3,750 tonnes for the year. Their replacement acid plant isn’t online until late 2026 at the earliest.

In Indonesian nickel, the feedstock for EV batteries, they need 25–30 tonnes of sulphuric acid per tonne of product. Huayou has already idled 50% of capacity. Indonesia sourced 75–80% of its sulphur from the Middle East last year.

China moved quickly to ban exports, but they’re not alone. Zambia implemented partial sulphuric acid export bans. Indonesia is redirecting domestically to protect local agriculture. There will be more.

What’s Already Happening at the Pump

The fuel picture is bad and getting worse. Diesel and jet fuel are at their lowest level in roughly 20 years: 102 million barrels. The US has been exporting oil at record pace to help allies, draining its own product stocks. The IEA confirmed global observed inventories are drawing at a record rate - 250 million barrels in April and May combined.

Truckload spot rates hit $3.61/mile on May 16, within $0.06 of an all-time record. Craig Fuller of FreightWatch called breaking it “inevitable.”

Diesel moves 70% of physical goods in America. Industry analysts estimate 6,000–10,000 small trucking carriers will exit the market if $6 diesel persists. When they go, logistics capacity contracts — and shortages spread to products that have nothing to do with oil.

Eric Nuttall of Ninepoint Partners — who went 100% oil-weighted in January 2026, before the war — said this on May 1:

“We’re not discussing months or quarters. Within the next few weeks, demand will need to be rationalized more than it was during COVID. This is undoubtedly the largest energy crisis that anyone living today has encountered.”

Supply will need to be rationed whether through price or actual allocation to “essential services” or both.

He’s calling for $150 crude to force enough demand destruction to rebalance supply. Brent is at $107. The distance between here and $150 is the distance between ‘expensive’ and ‘rationed.’

The Scoreboard: Price Changes Since February 28

The Sleeper Nobody Saw Coming: Motor Oil

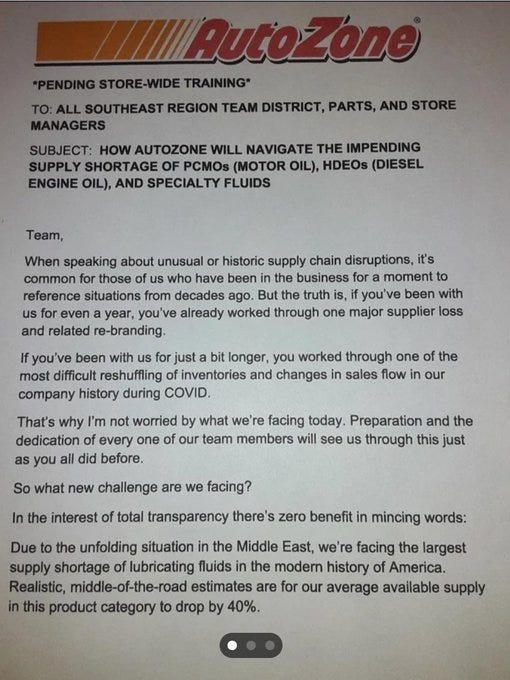

An internal AutoZone memo, corroborated by multiple independent sources, contains the following:

“We’re facing the largest supply shortage of lubricating fluids in the modern history of America. Realistic, middle-of-the-road estimates are for our average available supply in this product category to drop by 40%.”

Qatar, Saudi Arabia, and the UAE produce most of the ultra-high-quality synthetic base stock in virtually every modern motor oil. About 40% of global Group III production is now offline.

The ultra-thin viscosities required by most vehicles built after 2015 — 0W-8, 0W-16, 0W-20 — depend almost entirely on these Gulf base stocks. AutoZone is training staff on substitution protocols right now. Toyota has issued a service bulletin to dealers with blending guidance. Mobil and Shell reportedly told Costco and Walmart they’re out of product to ship.

For a trucking fleet already bleeding on $5.65 diesel, inadequate lubrication is not a nuisance. It’s a compounding existential problem.

The Food Shock Is Already Locked In

70% of US farmers say they cannot afford all the fertilizer they need this spring. In the South, 78%. Urea is up 49%. Anhydrous ammonia up 32%. And yet, Mosaic, the world’s largest phosphate producer, is losing money despite these surging fertilizer prices. Why? Supply chains. Mosaic’s acid input costs are rising faster than output prices.

The USDA has confirmed the lowest US wheat acreage in 107 years of recorded data. Farmers are cutting nitrogen-hungry wheat and switching to soybeans wherever they can.

Here’s the thing nobody in the mainstream is saying clearly: fertilizer applied in May determines the harvest in October. Fertilizer NOT applied in May also determines the harvest in October. That decision is being made right now, and no policy announcement between now and July changes it.

The food price shock you see today is the upstream cost signal. The actual grocery shelf impact hits in fall 2026 and runs through 2027. It’s baked in. The ovens are already on.

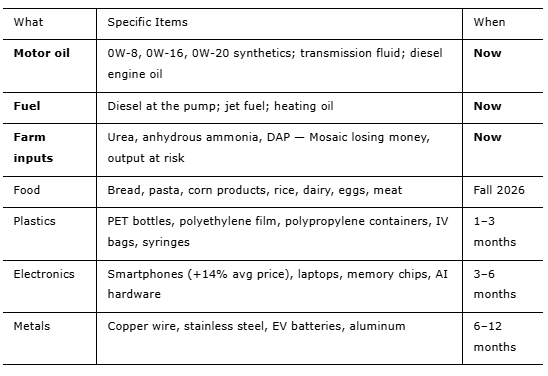

What You’ll Actually Run Short Of

The Reopening Won’t Save You

Here’s the trap most people are falling into: they think reopening the Strait means prices crash and shelves refill. Crisis averted. It doesn’t work that way.

The moment the Strait reopens, every country simultaneously tries to refill strategic reserves, commercial inventories, and supply chains. Demand surges an estimated 40%. If this happens, the price doesn’t drop on peace, it spikes on the buying stampede.

That’s why JPMorgan has Brent staying in the low $100s through year-end, even assuming a June 1 reopening.

And that’s the best case. Qatar’s Ras Laffan LNG and helium complex needs 3–5 years to reach full capacity again. Iraq’s older wells may never recover to pre-war output levels. The market hasn’t priced that yet.

Is the market pricing anything yet?

For sulphuric acid, copper, nickel, uranium, and food: the damage from the 2026 disruption runs multi-year regardless of what happens diplomatically.

A National Security Event Dressed as a Commodity Story

The US defense industrial base runs on copper, cobalt, uranium, and rare earths. All of them are processed with sulphuric acid.

If the political fight for scarce acid is won by the fertilizer industry the critical minerals pipeline for military hardware tightens. That’s a multi-year problem that we’re already seeing in the price of copper.

China controls 85% of global manufacturing for the specialized extractants required to separate rare earth elements. Energy Fuels (UUUU) White Mesa Mill in Utah, the only US facility processing rare earths from conventional sources, already has low supplier diversity for those chemicals.

This is not a commodity story. It’s a national security story with a commodity price tag.

The Apathy Problem

Nuttall said it plainly: “There is still a lot of apathy because people seem unable to fully grasp the situation.”

I get it. The shelves are still stocked. The pump still works. It’s hard to act when the product is still there - just $1.50 more per gallon. The human brain treats slow-moving catastrophes like background noise.

But the motor oil memo, the freight rate record, the 107-year wheat planting low, the Kazatomprom guidance cut — these aren’t forecasts. They’re data. The shortage is not coming. It’s here, in the upstream. It travels to the consumer at the speed of supply chains, which is measured in weeks and months, not years.

Supply chains are cracking and even a resolution to the war in Iran today won’t mean they’ll recover in time. And, yes, markets are still sleepwalking through what the data is already screaming.

What This Means For YOU

The question isn’t whether this affects you. It’s whether you’re positioned for it.

That’s what Crisis Investing is about. Every issue identifies the dislocations, names the assets, and gives you a framework for acting before the crowd figures it out.

Here’s the hard truth: most companies touched by this cascade will be crushed by it. The trucking carrier that can’t absorb $6 diesel. The copper miner that can’t source acid at any price. The fertilizer producer whose input costs outrun its revenues — like Mosaic, the world’s largest phosphate producer, losing money into a fertilizer price spike.

But a handful of companies are positioned to do the opposite. They don’t just survive the shortage — they profit from it. One large-scale copper producer, for example, generates its own sulphuric acid on-site and sells the surplus into a market where prices have risen 158% in ten weeks. While its competitors scramble for supply, it’s collecting the windfall. That’s not luck. That’s structure.

Finding that structure — before the crowd — is the entire purpose of Crisis Investing. The shortages are already in the data. The companies that benefit already exist. The window to position ahead of them is measured in weeks, not months. Look out for the next issue of Crisis Investing where we’ll reveal the names.

If you’re not a subscriber, now is the time.

Matt Smith

Crisis Investing

Great article Matt. But you're such a tease! Who is the Copper refiner that produces its own sulfer? Or will you and Doug be showcasing that company in another episode? It's nice to have level headed analysis of the stuff going on, and not the rah-rah bs from most sources.

Really top notch analysis here Matt. Keep it coming and please keep warning people. Some disasters you can see far away. There's still a "cone of uncertainty" that could allow this to resolve in a much better fashion, but I'd rather not get caught with hopes and dreams as my primary plan.