Congress Fixed Housing

Okay. I’m lying about that.

A housing bill.

It sounds like something Hollywood writes to make an actor playing a politician look like a good person. Michael Douglas is lauded for a bill cutting fossil fuel emissions twenty percent. Kevin Kline rewrites the federal budget at a kitchen table one night and then fights for a national job guarantee. Charlize Theron saves the seas, the bees and the trees with a 100-nation treaty.

Naïve foolish idiotic drivel that moviegoers are emotionally programmed to venerate.

Then the credits roll and you never see the second act, where the asinine economic fantasies of Hollywood meet arithmetic.

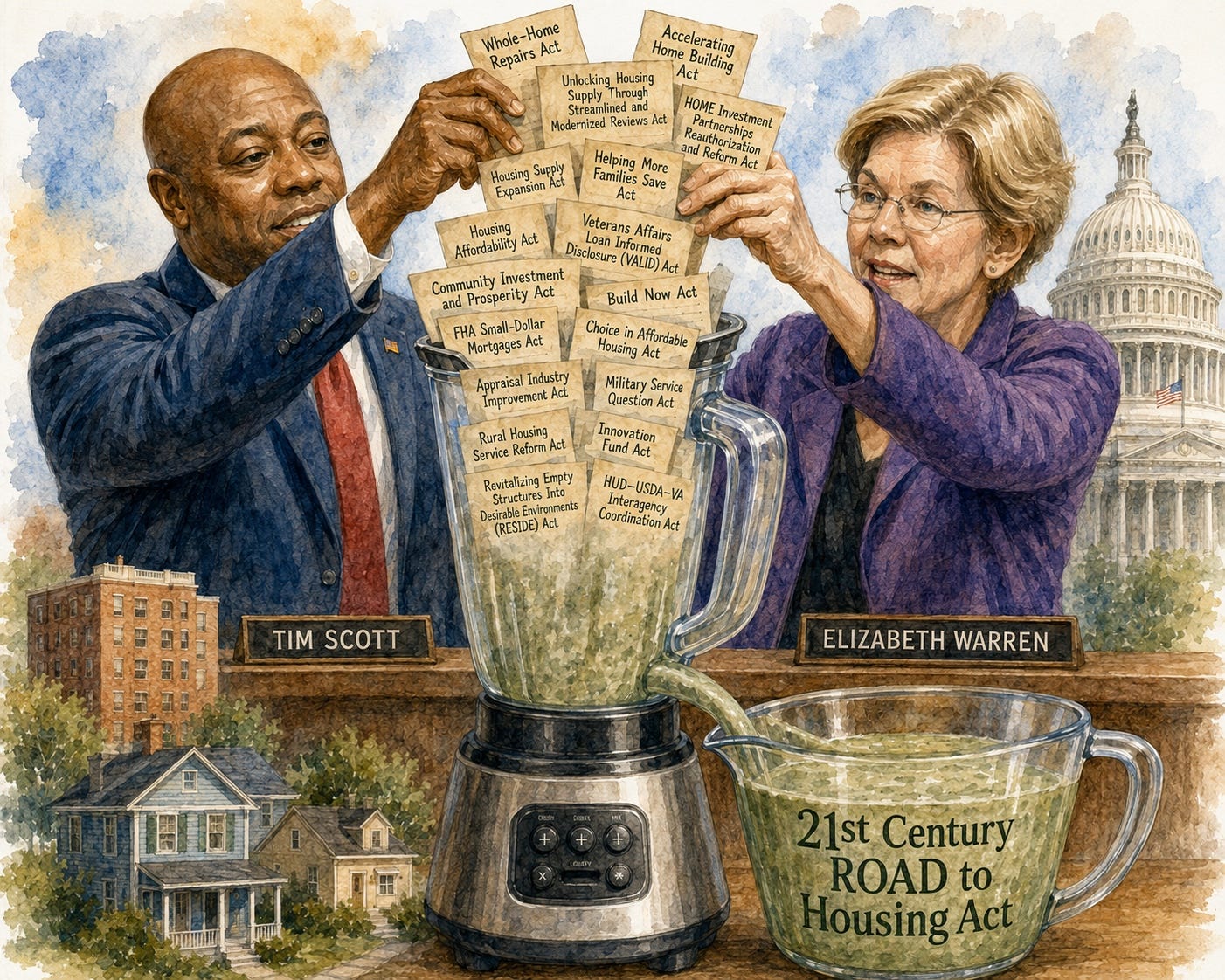

This brings us to the 21st Century ROAD to Housing Act, which runs twelve titles, sixty provisions, and 56,025 words, mashed together from sixty separate bills. Elizabeth Warren (D) and Tim Scott (R) stuck them all in a blender and made a slushie. The Senate voted 85-5. The House voted 358-32.

The three letters CON appear in this housing act 573 times. Yet the term Constitution appears zero times. Zero mentions. No thought given to whether this act might be among the enumerated powers of Congress.

The only parts of this act that work are the parts that stop government

A few provisions do good work.

The law kills the permanent chassis requirement Congress wrote in 1974—a rule that forced builders to weld a steel frame under a house that would never move again, so it could qualify as a trailer. Removing it cuts a bit of cost from producing that type of home. Also, HUD will write guidelines letting states permit six-story buildings with a single staircase, which Europe has done for ages without bodies stacking up. And environmental review gets carve-outs for infill lots.

Each one is government stopping something it should never have started. No appropriation, no metric, no program officer, no forms needed. Congress repealed bad rules. It’s like a tiny chainsaw, cutting some tiny sticks.

They also threw in a ban on Central Bank Digital Currencies, a rider that has nothing to do with housing but that makes the bill worthwhile, a bit. The ban sunsets December 31, 2030, so the Fed could build the diabolical thing now and wait. Conspiracists may circle January 1, 2031 as the day the Fed could take control over your entire economic life. But, for now, total economic control gets deferred for a few years. I’ll take that as a bit of a win.

Add up every good word in this law that stops government from doing something: 3,542. Out of 56,025 words total. Six percent.

The rest of the words expand government involvement. Of course.

Trump’s 350 house max

Title 10 bans institutional investors that own 350 or more single-family homes from buying any more. This is the headline, the part smarmy politicians can run on. Trump called for this cap back in January. Keep in mind the large institutions own less than 1% of these houses.

Manufactured homes are exempt from the arbitrary 350 cap. Congress cut the cost of a manufactured house in Title 3 and left it open to unlimited institutional buying in Title 10. Politicians are picking and choosing winners and losers again.

Investment capital doesn’t disappear because Congress outlaws one destination. It simply flows into the next most attractive legal alternative. Capital that cannot legally buy a 351st stick-built house instead buys manufactured homes, a fourplex, a condo, a tower—basically unlimited properties that shelter families from the weather while sheltering corporations from the whims of the lawmakers. There will be some effects of this on the composition of the housing market, although it may not change the American Dream.

And there is a grandfather clause. Existing institutional holders of single-family homes get to keep them. The law just forbids anyone else from joining them and propagandizes it as protection for families.

The ban repeals itself fifteen years after it takes effect. Maybe 350 will not be Trump’s special number by then?

The demand pump

The law expands FHA credit. Small-dollar mortgages under $100,000. Higher loan limits on multifamily and manufactured housing. Every one of those provisions raises what a buyer can bid. To the extent the loan-subsidized (and therefore higher) prices encourage new construction, then they get what they intend.

But where supply cannot respond (because zoning, land, and labor bind it), additional purchasing power from easy credit does not build additional houses. It becomes additional price. The buyers get more debt to pay off and a higher risk of foreclosure.

More slop added to the slushie

Section 107 abolishes the Regulatory Barriers Clearinghouse - a HUD office created in 1992 to collect and publish information on the regulatory barriers that make housing expensive. Section 107 then spends 1,275 words ordering the same HUD office that ran it to convene a task force of urban planners, architects, and “community engagement experts” to publish guidelines and best practices on the regulatory barriers that make housing expensive. Looks like the HUD office workers won’t lose their jobs, but maybe they’ll get a new name for their work.

Section 106 spends 1,108 words on a pilot program to install internet-connected temperature sensors in federally assisted apartments. These are to be accurate to a tenth of a degree. Big Brother will keep an eye on whether these folk are warm, and with precision too! The program sunsets after three years, which is about when HUD will finish defining the rules.

Legislated studies, reports, and mandatory testimony requirements run 5,925 words—more than the 3,542 words that are in this law that did anything good.

And there is a bunch of other hogwash among the pet bills that lobbyists have been trying to get Congress to pass. It’s all in Warren and Scott’s blended slushie.

Although the law authorizes $1 billion for an innovation fund and the slushie of 60 provisions involve added bureaucracy and reporting, the very end of the law says that “No additional funds are authorized to be appropriated to carry out the requirements of this Act or any amendment made by this Act.” Maybe they are relying on Modern Monetary Theory to conjure up the spare dough.

Unpredictably unpredictable

It’s kind of a fool’s game trying to predict how Congress pushing this button or that one is going to fall out in the housing markets or the stock markets. Throw in a dollop of President Trump and it’s all a quagmire of criss-crossing spaghetti noodles.

We already know that Congress is lousy. We already know that when Congress does something, it is, on net, harmful. They wield power unconstrained by the Constitution.

Few congressmen understand economics. Few think soundly. Few obey their oath of office.

Few Americans have the time—or the inclination—to read 56,025 words of federal legislation. So we don’t read it. We just take a feeling that was installed in the news, or in a theater, perhaps by Michael Douglas.

We are supposed to think: Housing Bill. Bipartisan. Bipartisan means Unity, America, Good. A good housing bill. Good politicians. Let’s re-elect them.

But I actually read the bill. It didn’t make me think that. It made me think of Idiocracy.

John Hunt, MD

Editor, Doug Casey’s Crisis Investing

They need to drastically free up the supply of homes available for purchase to put downward pressure on prices. Increase the federal deduction on the gain of a home sale so boomers and their heirs don’t have to wait for the boomers to die to sell.

Also, return most of the federal lands back to the states.