U.S. Debt Just Crossed $39 Trillion

And There's Only One Way This Ends

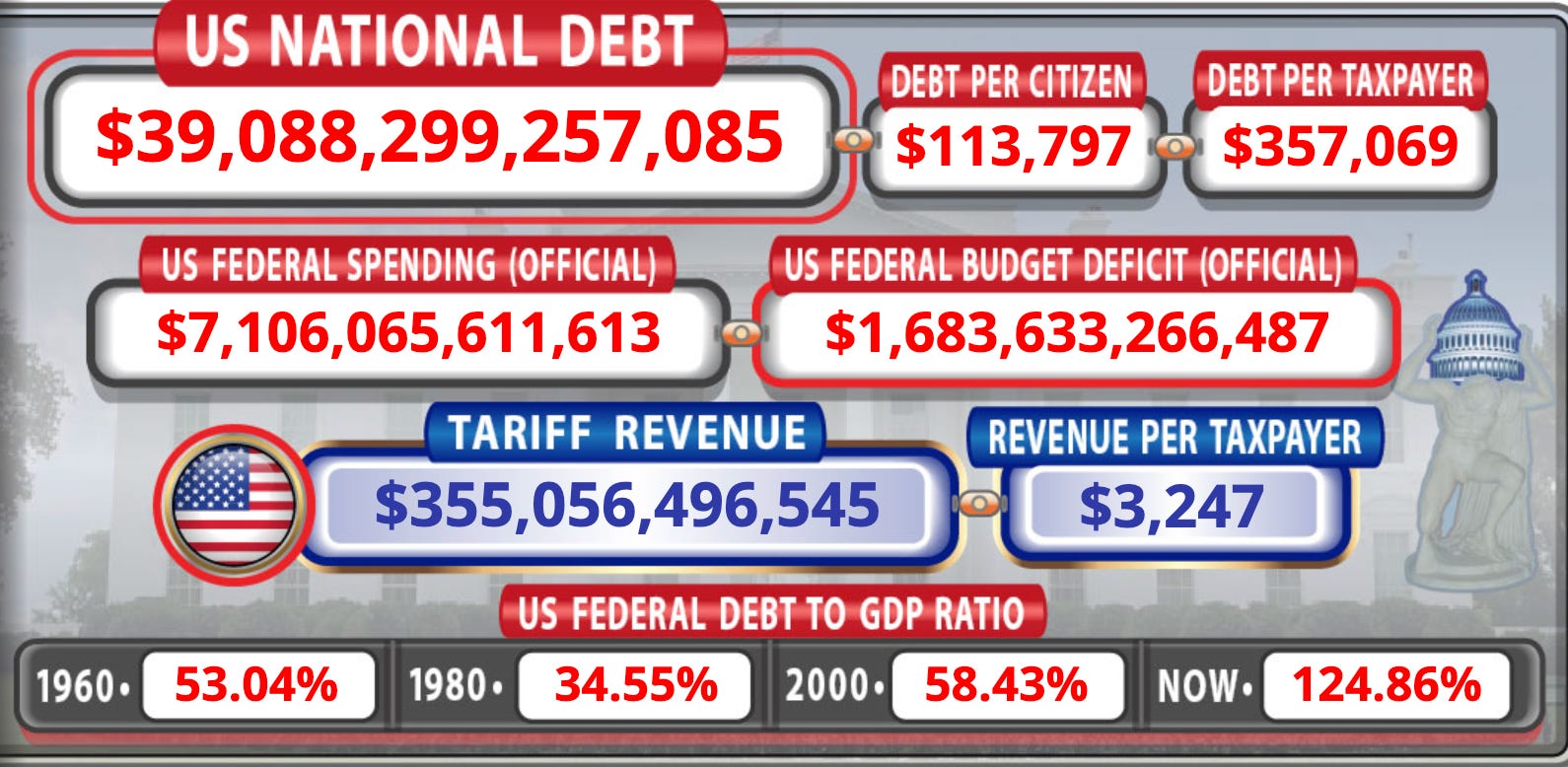

The U.S. has just smashed through another historic fiscal milestone — $39 trillion in national debt. That’s roughly $357,000 for every U.S. taxpayer and nearly $114,000 for every American citizen.

But the headline number isn’t what should worry you. It’s the pace.

In January 2024, the national debt stood at $34 trillion. By August 2025, it crossed $37 trillion. By late October, $38 trillion. And now, $39 trillion. That’s another $1 trillion piled on in roughly five months.

Back in September, I wrote that on the then-current trajectory, $40 trillion would arrive by late 2026. Turns out I was being conservative. At the current run rate, $40 trillion will be here before the end of fiscal year 2026 — September 30. Maybe sooner.

That’s because Washington is now adding debt at a rate of about $8 billion every single day. Roughly $340 million every hour. Nearly $5.7 million every minute. You can step into the bathroom, and by the time you walk out, the U.S. will be another $25 million deeper in the hole.

And remember — this is all happening at a moment when there’s no pandemic, no financial crisis, nothing on the scale of anything in the postwar record to “explain” it. In fact, the recent explosion in U.S. debt is unlike anything we’ve seen in the historical spikes during major wars and financial crises like the Civil War or World War II. There’s no single exceptional event driving it. This time, the crisis isn’t a moment — it’s the system itself.

The Broken Promise

There’s an irony here that’s worth naming.

Before returning to the White House, Trump promised to pay off the national debt. Not reduce. Not stabilize. Pay it off. Instead, the debt has climbed by trillions — and has now nearly doubled from where it stood when he first took office in 2017. The DOGE effort that was supposed to take a chainsaw to spending got rounded down to a rounding error. The “Big, Beautiful Bill” added trillions in projected new deficits over the next decade. And now an Iran war that nobody budgeted for is layering its own bill on top of all of it — with the Pentagon already hitting up Congress for another $200 billion in supplemental war funding.

But the war supplemental is just the opening act. The real number is what’s happening to the military budget itself. The White House has proposed jumping FY2027 military spending from roughly $840 billion to $1.5 trillion — a nearly $700 billion increase in a single year. That is, by a wide margin, the single largest year-over-year military spending increase since World War II.

Stack all of that on top of a baseline where the Congressional Budget Office (CBO) is already projecting a $1.9 trillion federal deficit this fiscal year, climbing to $3.1 trillion a decade out — and remember, every dollar of deficit is another dollar piled onto the debt — and you start to see the picture. Every one of those projections assumes no new wars, no new recessions, no new emergencies. And it already looks catastrophic. The reality is almost certainly going to be worse.

Put plainly: on every metric that matters — deficits, debt, interest costs, new obligations being added — the U.S. fiscal picture has never been worse than it is right now. Not in the 1970s. Not post-2008. Not even during COVID. Right now.

And then there's the interest bill.

Net interest payments on the federal debt are now projected to exceed $1 trillion in fiscal year 2026 — nearly triple what the government paid in interest in 2020. That makes interest on the debt the second-largest line item in the federal budget, behind only Social Security. Bigger than Medicare. Bigger than the military.

Think about that for a second. The largest single thing the U.S. government now spends money on is interest on money it has already spent.

It boggles my mind that we don’t wake up to this on the front page every day — especially now that the bond market has started to notice.

The 10-year Treasury yield jumped roughly half a percentage point in a matter of weeks — pushing above 4.45% — as recent Treasury auctions came in weak, with buyers demanding higher yields just to absorb new issuance. This matters for one simple reason: the U.S. government has to roll over close to $10 trillion in debt this year. Every tick higher in yields means every dollar of that refinancing costs more. And more. And more.

Now, I’m not saying the U.S. will default outright — that would be political suicide for those at the top. The only alternative they have is to inflate it away. That means devaluing the dollar — quietly, persistently, and on a scale that makes the post-2008 money-printing era look like a warm-up.

Devalue or die. There is no third option.

Regards,

Lau Vegys

P.S. And it’s about to get much worse. The traditional foreign buyer base for U.S. Treasuries is about to come under enormous stress — all at once. Saudi Arabia, the UAE, and Kuwait together hold over $1 trillion in U.S. financial assets, and with Hormuz effectively closed and their oil revenues collapsing, they’re about to become forced sellers. Japan — America’s single largest foreign creditor, with $1.2 trillion in U.S. Treasuries alone — is getting crushed by the same energy shock: it imports nearly 90% of its energy, and two-thirds of its oil supply is currently blocked. We walk through all of it in our latest issue of Crisis Investing, published last week — along with two new recommendations built on exactly this thesis. Even if you're not yet on the paid side, the lead — featuring Doug Casey's latest words of wisdom — is free to all.

Keep stacking my friends. This ends badly

But it’s not real money which makes up the Debt. It’s monopoly money. Yes, the monopoly money becomes worth less every day. The so called ruling class likely deploys a lot of the monopoly money into hard assets. Quite a game.