The Auto Loan Crisis Nobody’s Talking About—And How We’ll Profit From It

'Crisis Investing' Issue 11 / November 2025 – Vol 2

Dear Reader,

Americans owe $1.66 trillion in auto debt.

That’s trillion with a T. To give you an idea of how crazy that is, it’s even slightly more than the scandalous levels of student loan debt (at about $1.65 trillion). And right now, a product once considered one of the safest in consumer credit is quietly becoming one of the riskiest.

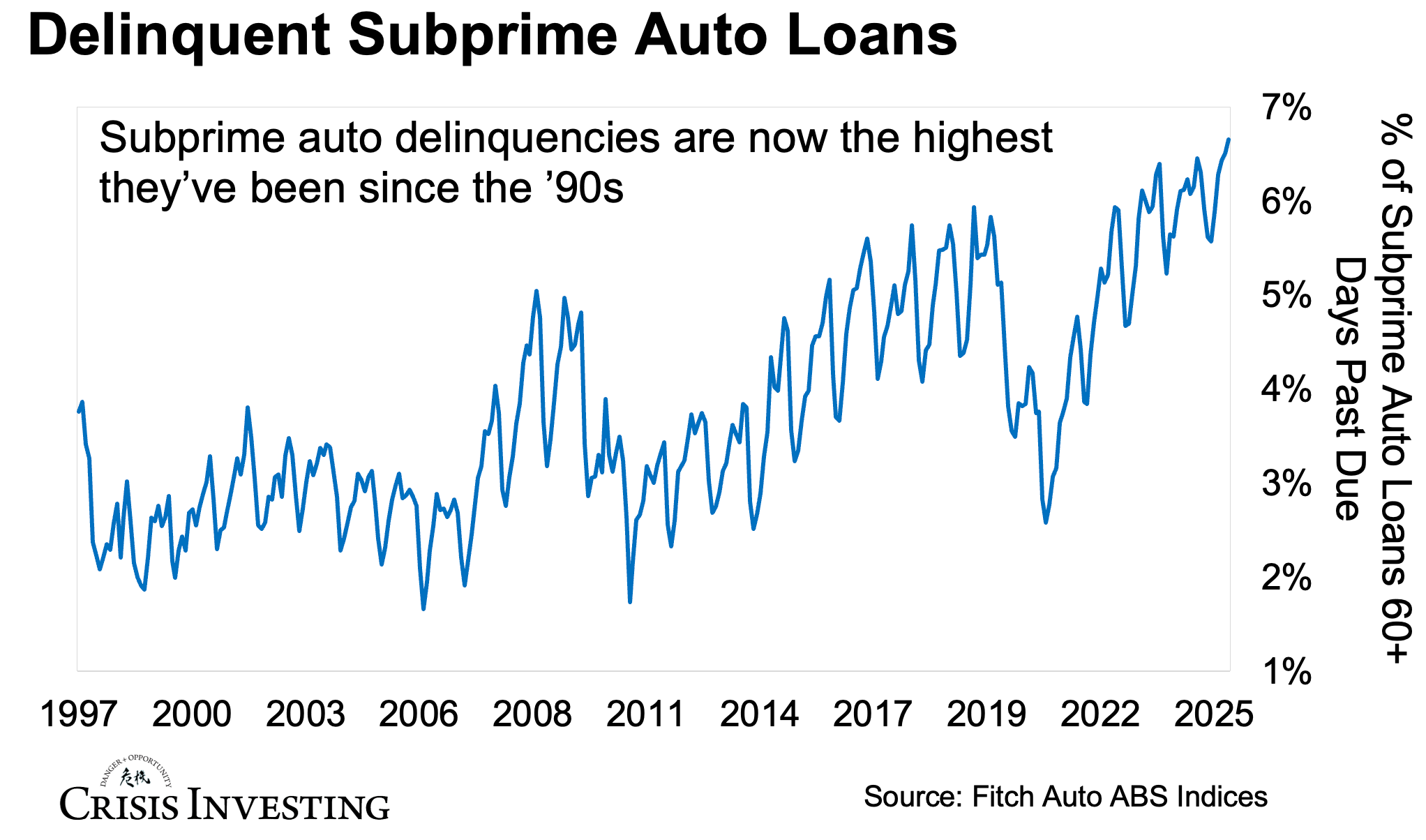

For one, auto loan delinquencies just hit levels we haven’t seen since the Great Financial Crisis. Take a look at Fitch Ratings’ auto loan delinquency index:

Subprime borrowers are getting crushed, with 6.65% of loans at least 60 days delinquent as of October 2025. That’s the highest level in over 30 years—worse than anything we saw during the Great Financial Crisis.

Even prime and super-prime borrowers are starting to crack. Severe-stage delinquencies among super-prime borrowers have more than doubled year-over-year. When your best customers start missing payments, something fundamental has broken.

Meanwhile, the average monthly payment for a new car now exceeds $750. For used cars, it’s $540. Average loan amounts have hit $41,983 for new vehicles and $26,795 for used ones. Many borrowers are locked into 7-year loans—that’s 84 months of payments on a depreciating asset.

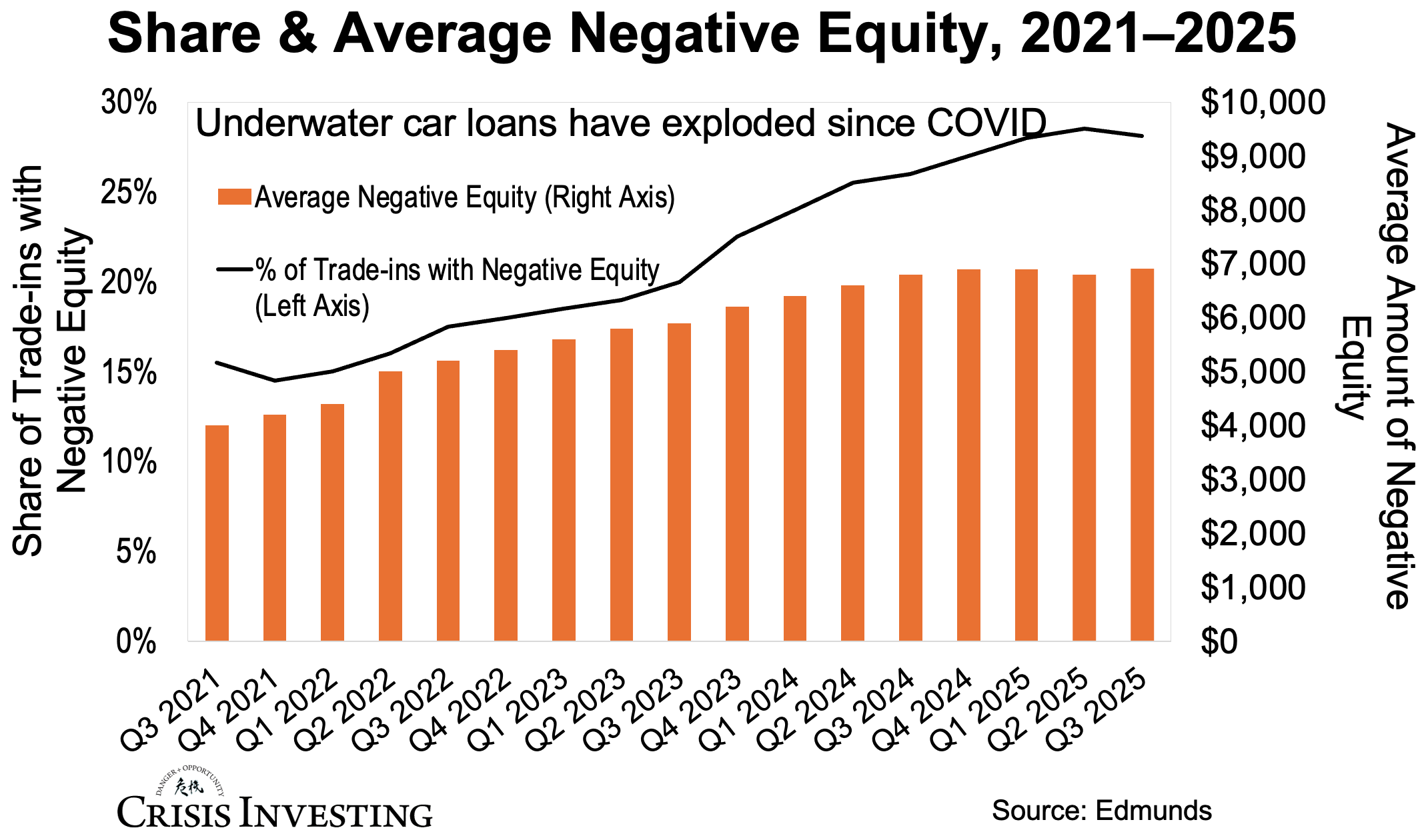

And it gets worse. A growing number of car buyers are underwater, owing more on their loans than their vehicles are worth. Take a look at this chart from Edmunds—one of the leading automotive data and pricing firms—tracking the share of trade-ins with negative equity and the average amount owed over the vehicle’s value:

Nearly 28% of all trade-ins are now underwater—meaning more than 1 in 4 car owners owe more than their vehicle is worth. And the average amount of negative equity has surged to almost $7,000, up from around $4,000 during the pandemic lows.

So why is this happening?

Once again, it all goes back to the COVID years—the peak era of loose lending standards, inflated vehicle prices, and stimulus-fueled demand. Used car prices spiked more than 50% as supply chains collapsed and new-car production froze. Buyers paid whatever they had to, financed at whatever rate they could get, and many dealers pushed loans that should never have been written.

Now those inflated prices are coming back to earth, but the loan balances aren’t. When car values depreciate faster than loan balances decline, you get trapped. You can’t sell without taking a loss, and you can’t refinance into better terms.

Note: The Fed’s own research confirms what many suspected: loans originated in 2021-2023 are performing terribly.

Meanwhile, the broader economy has been showing serious cracks. As stimulus money faded and interest rates reset higher, reality started to bite. Real wages haven’t kept pace with inflation. Savings built up during the pandemic are gone. Credit-card balances are at all-time highs, and delinquencies are rising across the board.

The point is, consumers are stretched thin—and when tough choices have to be made about which bills to pay, the car payment increasingly gets pushed to the back of the line.

In other words, the chickens are finally coming home to roost.

The data backs this up. According to VantageScore—one of the major U.S. credit-scoring firms—consumers are now “prioritizing their debt obligations, and auto loans are decreasing in priority.” Translation: people are choosing to pay their mortgages and credit cards first, letting their car payments slip.

The Consumer Federation of America put it bluntly in their recent report: U.S. auto financing is at a “breaking point.”

They’re right about that. Because here’s the thing about systemic problems in consumer credit markets: they don’t resolve themselves gently. They break. Companies built on shaky foundations of overleveraged consumers and questionable lending practices tend to come apart fast once the tide goes out.

For contrarian investors who understand crisis, this kind of environment creates real opportunity—to profit from the unwinding of business models that were never built to last.

Below, in this month’s issue of Crisis Investing, I’ll walk you through a company that Doug, Matt, and I uncovered—one that embodies everything wrong with this market—and how to position yourself to profit when it all comes apart.

Happy investing,

Lau Vegys