Japan Is Broke—and It’s America’s Problem

How Japan's Crisis Could Trigger the Next Financial Meltdown

What if I told you that something bad is happening with the U.S. government's biggest creditor on Earth—and it could have very serious implications for your portfolio?

This story caught my eye a couple of weeks ago, and I've been meaning to write about it but kept pushing it to the backburner because I had my plate full at the time. But it's too important to ignore any longer.

So what's going on?

Last month, Japan's Cabinet Office published their latest economic figures, and they were not good. Japan's economy shrank for the first time in a year, contracting by 0.7%.

That's bad news, especially since it happened even before the bulk of President Trump's tariff measures took effect. Now it's almost a given that Japan will continue shrinking this quarter, which would put the country in a technical recession.

I realize you probably don't spend much time thinking about Japan's economy. Most people don't. It's on the other side of the world and doesn't dominate headlines like the U.S. or China.

But Japan isn't just any country. It's one of the biggest creditors on Earth.

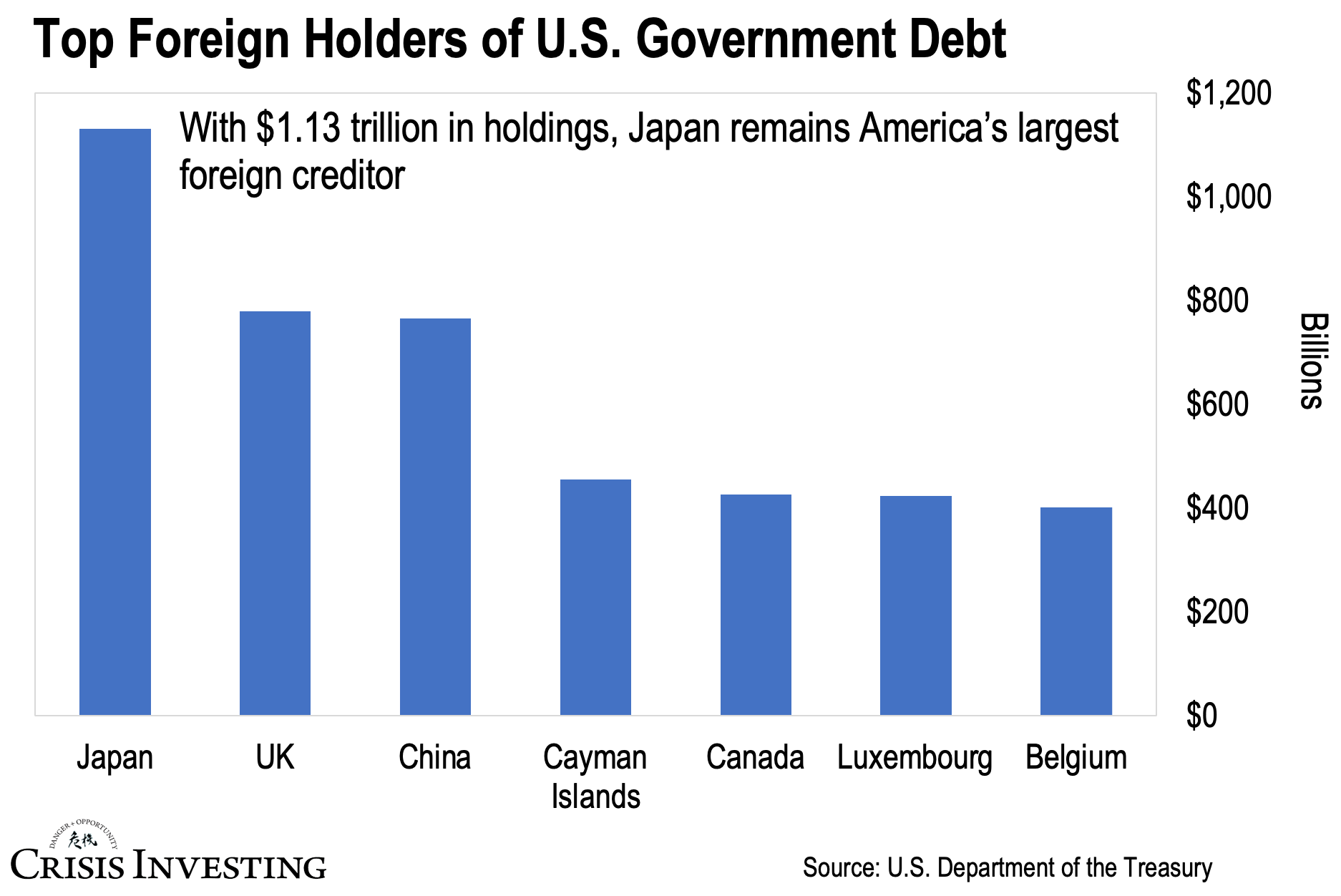

Japan holds over $3 trillion in net foreign assets and is the top holder of U.S. Treasuries—over $1 trillion as of 2025. Take a look at the graph below.

And it's not just bonds. Japanese institutions have billions tied up in U.S. stocks, corporate debt, and real estate.

But what happens if Japan suddenly needs to call that money home?

It would send shockwaves through global markets—driving up interest rates and making borrowing far more expensive for everyone. And because Japan has its fingers in so many pies, it wouldn’t just rattle Wall Street… it could light the fuse for the next global recession.

Japan’s Many Problems

To understand why Japan can actually crash global markets, you need to understand the precarious situation the country is in. And it goes well beyond one quarter of negative growth.

Japan is facing a deepening population crisis. The nation's population has declined for 15 consecutive years as fewer people marry and have children.

That's not unusual—many developed countries are grappling with falling birth rates.

But not every developed country has the third-lowest fertility rate in the world. Japan recently hit a record low of 1.15, down from 1.2 the year before—the lowest since record-keeping began in 1947.

Keep in mind, you need a fertility rate of about 2.1 to maintain a stable population.

To make matters worse, Japan also happens to be the oldest country in the world. About 30% of its population is over the age of 65.

Combined, these factors mean that by 2050, Japan is projected to lose around 20 million people—about 16% of its current population. And by the end of the century, the country is expected to lose more than half its population. That's like the entire state of Florida vanishing now, and most of the United States East Coast disappearing later.

This crisis affects far more than retirement homes and hospitals—it's crushing the entire economy.

Fewer workers means less growth. More retirees means rising government spending. Every below-replacement-level country faces these problems, but when your fertility rate is plummeting toward 1 and you have the oldest population on Earth, you’re dealing with a whole new level of crisis.

The government's solution to keep the system afloat?

Borrow money. Lots of it.

For decades, Japan has borrowed like there's no tomorrow, which is why it now has the highest debt-to-GDP ratio in the developed world: over 260% and rising.

It was the same familiar playbook: keep interest rates at zero and have the central bank print money to buy government debt.

And for years, Japan got away with it.

Then reality came knocking.

When Math No Longer Works

You might remember Monday, August 5th, 2024. Calling it a bad day in the markets doesn’t even begin to cover it. Japan’s benchmark Nikkei index plunged 12.40%—its worst single-day drop since Black Monday in 1987.

The sell-off started in Japan but quickly spread across Asia, then Europe, and finally the U.S. All told, over $5 trillion in global market value was wiped out in just one day.

And it wasn’t just stocks. Oil, other commodities, Bitcoin—you name it—everything got hit.

But more striking than the losses was the speed. Things unraveled so fast that even seasoned market pros were caught off guard.

The trigger behind the global meltdown was a financial powder keg known as the yen carry trade.

Here’s how it works…

In a yen carry trade, big institutions borrow Japanese yen at rock-bottom interest rates. Then they convert that cheap money into dollars and plow it into higher-yielding assets abroad, especially in the U.S.

Imagine you're a trader who borrows 10 million yen when the exchange rate is 100 yen to the dollar. That gives you $100,000 to play with. You dump this money into U.S. Treasury bonds yielding 4%. After a year, you've pocketed $4,000 in interest. And it gets even better—if the yen has weakened to 105 yen per dollar, you only need $95,238 to repay your loan. You've profited not just from the interest rate difference, but also from the currency move.

It's essentially free money. At its peak, Bloomberg estimated yen carry trades reached hundreds of billions globally. Traders had been milking this cash cow for decades. Some people called it "the global money glitch."

But there’s a (predictable) catch.

This strategy only works as long as Japanese interest rates stay low and the yen remains weak.

If either goes the wrong way, the trade breaks.

That’s exactly what happened in 2024. After nearly two decades of keeping rates near zero, the Bank of Japan finally blinked—raising rates from negative territory to 0.25%. That alone sent the yen surging 10% in a matter of weeks.

Suddenly, the math flipped. Traders now needed more dollars to repay their yen-denominated loans than they had borrowed. That triggered a violent unwinding of positions—and a cascading sell-off across global assets.

The rest is history.

Just a Preview

Now, the Bank of Japan didn’t raise rates out of the goodness of its heart. When you have $8.5 trillion in debt—over 260% of GDP—even tiny rate increases are brutally expensive.

They were forced to.

Bond investors had started demanding higher yields. Japan’s auctions had begun failing. The BoJ, already holding 50% of the government bond market, found itself buying alone. Foreign and domestic investors were either fleeing or demanding much higher rates to offset inflation and currency risk.

So the BoJ capitulated.

And with Japan’s problems in 2025 looking worse than in 2024, rates will probably keep climbing—whether they like it or not.

The alternative is even more trouble selling their debt—along with a yen free fall that would make imports ruinously expensive. And I do mean ruinously since Japan imports 60% of its food and nearly all of its fossil fuel energy.

But rising rates in Japan spell trouble for the U.S.

Remember, Japan holds over $1 trillion in U.S. Treasuries—more than any other country. As Japanese rates rise and the yen strengthens, parking money abroad gets a lot less attractive. Instead of financing America’s debt binge, that capital will stay home.

Japan’s finance minister recently even floated the idea that their U.S. Treasury holdings could be “leverage” in trade talks. He later backtracked—but the message was clear: nothing is off the table in hard times.

Losing America's biggest creditor would crush America’s global credit standing, hammer the dollar, and drive up borrowing costs across the board. That would translate into higher interest rates for consumers, a paralyzed economy, and a brutal market collapse.

When August 5th, 2024 hit, I was struck by how violently U.S. markets reacted to events in Japan. The speed and scale of the sell-off were unprecedented outside of the COVID crash in March 2020.

I now strongly believe that was just a preview.

Regards,

Lau Vegys

P.S. If you ever needed proof that Japan matters on the world stage, just look back at what happened in 2010. A maritime clash with China turned into a full-blown rare earths embargo. I walk through the story in the latest Crisis Investing issue. That part of the lead is available to free subscribers—check it out. Some interesting charts in there too.

The bullion and stock accumulations recommended. How do those line up with wealth/net asset categories?

Like if someone had 250k in assets: buy x

Thanks