Dear Reader,

The biggest change since we last caught up is, of course, that Donald Trump has been elected to lead the world’s most powerful economy—the one that backs the almighty U.S. dollar.

Well, maybe not so mighty after all, considering everything going on around the globe right now. But, still, the dollar (and stock market) did get a bump after Trump won.

The interesting thing is that the same thing occurred last time Trump was elected—and we all know what happened after the first few weeks. Those gains evaporated real quick.

Still, I’ve had some people tell me, after Trump got elected, “Well, now that he’s in, I’m not worried anymore. I’m not going to invest in gold as much, or heck, I might even sell some.”

I think that’s absolutely crazy talk. Do you really believe the U.S. government is going to stop spending money? Do you think inflation is just going to disappear? Of course not.

This is exactly why the knee-jerk reaction to Trump's victory was an increase in the yield—essentially the interest rate—on U.S. government bonds. Bond yields tend to rise when investors expect higher inflation or larger budget deficits. Not great for the general population, but definitely great for gold.

The Big Picture

But why did it sell off after Trump’s victory then?

Once again, it all comes back to the “almighty” dollar. Gold sold off because traders believed the U.S. dollar would strengthen against other currencies. Doug Casey calls it the “prettiest mare at the slaughterhouse,” and right now, that's exactly what's happening.

As a side note, it's important to remember that gold also dropped sharply after Trump was elected the last time. That turned out to be a market bottom that hasn’t been revisited.

But back to the issue at hand... Just because the dollar is rising against the euro and other fiat currencies doesn’t mean it’s becoming more valuable. The latest U.S. CPI data shows it’s still losing purchasing power, despite what the economic cheerleaders say about inflation being under control. It simply means forex traders are anticipating more demand for dollars in the short term.

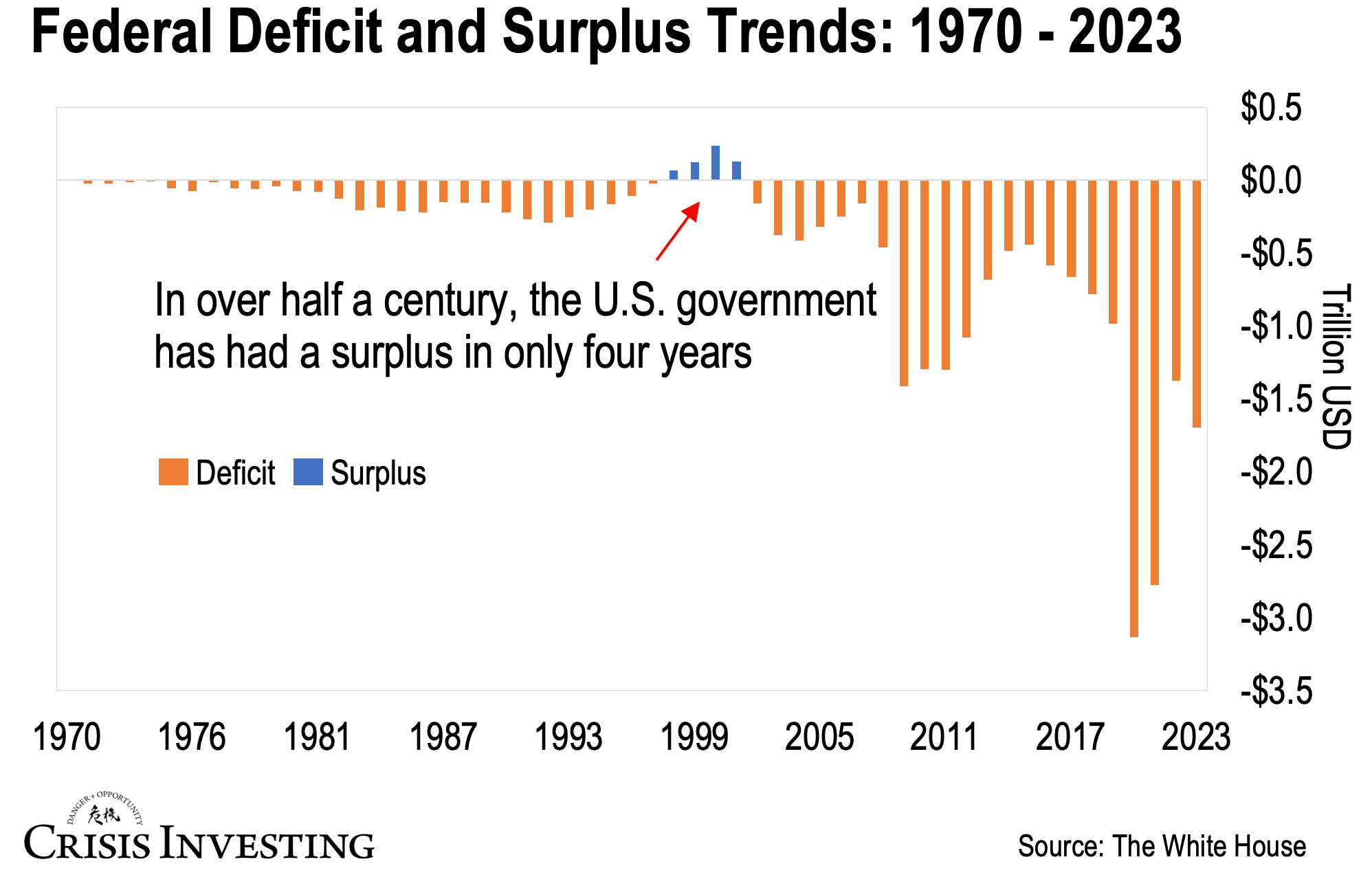

But, as any resource investor worth their salt knows, it's not the “short term” that should be your focus. You should be betting on a solid trend… like the one below, which you might have already come across in these pages before.

As you can see, since 1970, the U.S. government has consistently run deficits, with only a few exceptions. Each time, it piled on more and more debt. Every single time.

Even the last so-called "balanced budget" under Bill Clinton (see blue bars above) largely resulted from accounting tricks, and the debt still increased during that period.

The point is, regardless of who occupies the White House, each administration spends more than it collects and breaks the previous debt record. That's what our government does.

Now, I'm glad Trump won. Not because I'm enamored with the guy—I'm cautiously optimistic at best. But because the alternative was so, so much worse. Still, the U.S. government will keep spending and printing dollars no matter who is in office.

So I'm betting on the continued deterioration of the U.S. dollar's purchasing power, irrespective of what Trump does.

Dishonest Default

Not convinced? Let’s break it down. The U.S. government’s on-balance sheet liabilities just topped $36 trillion. To put that in perspective, U.S. GDP is around $31 trillion.

But that’s not all—there’s also another $100 trillion in unfunded liabilities (things like Social Security, Medicare, and Medicaid). All together, that’s a staggering $136 trillion. For comparison, the IRS reports Americans’ total net private wealth is about $141 trillion, so the national debt is nearly on par with the country’s entire private net worth.

This is bad enough, but it actually gets worse...

The on-balance sheet debt grows by $2.5 trillion a year, while the off-balance sheet liabilities are adding another $3 trillion annually. That means the debt is increasing by $5.5 trillion each year, which just happens to be the same amount as the U.S. government’s total gross revenue. So we’re growing the deficit at the rate of 100% of the government’s revenue, year after year. How is this sustainable? It’s not.

There are only two ways out of this mess. One is an honest default, basically saying we can't pay the debt. I agree with Doug that this would be the moral choice. The other is a dishonest default, where they just inflate the debt away. Guess which option the politicians will go with?

In fact, they did this back in 1971. The government had unsustainable spending and off-balance-sheet liabilities, and raising taxes was off the table. So, what did they do? They inflated away the value of those obligations, reducing the purchasing power of the U.S. dollar by 75% from 1970 to 1980.

This wasn’t the first time, though. As you probably know, the government also devalued the dollar in 1933. They did this by ditching the (domestic) gold standard and raising the price of gold from about $21 to $35 per ounce. That devalued the greenback by roughly 40%.

So, if history is any indication, they’ll do it again.

Sure, the government will keep paying the check—let’s say a retired guy named Bob, who’s collecting Social Security, will still get his $1,800 a month. That won’t change. But while Bob will still see the same number on his check, what that money actually buys will shrink dramatically. So, Bob’s $1,800 might sound nice, but with inflation, it'll only be worth about $600 in terms of what it can actually purchase. He’ll still get the same payment, but it won’t stretch nearly as far.

Gold Comes Through

So, what does all that have to do with gold?

Well, in the 1970s, as the dollar lost 75% of its purchasing power, gold skyrocketed from $100 to $850 per ounce. That’s a rise of 8.5 times.

And just to be clear, I'm starting at $100, not the earlier $35 price, which was an artificial government-imposed cap that held gold back for decades.

Now, don’t get me wrong, I’m not saying we’re going to see an eight-fold increase in gold over the next decade. But, as you know, history doesn’t exactly repeat, but it sure does rhyme.

For perspective, gold was trading at a mere $250 per ounce back in 2000. Flash forward to today, and it's sitting at around $2,600. That’s a seven-fold jump. If you do the math, that’s an 8% compounded annual return over the past 24 years.

What does that tell us? Gold has done exactly what it’s supposed to do: it’s maintained its purchasing power. And honestly, that’s what I expect it to continue doing going forward.

The takeaway? Keep investing in gold and silver, no matter who’s in the White House. I’m confident you’ll make a solid return in the long run.

Now that we’ve covered the big picture, let me share some quick thoughts on Trump’s agenda and what it could mean for gold in the coming months—especially since I’ve got an exciting new gold pick for you today.