Coal Was Already Coming Back—Before Hormuz Even Closed

Chart of the Week #105

A few weeks ago, we published our latest issue of Crisis Investing — built around the contrarian argument that coal never went away, no matter how many funerals were scheduled for it.

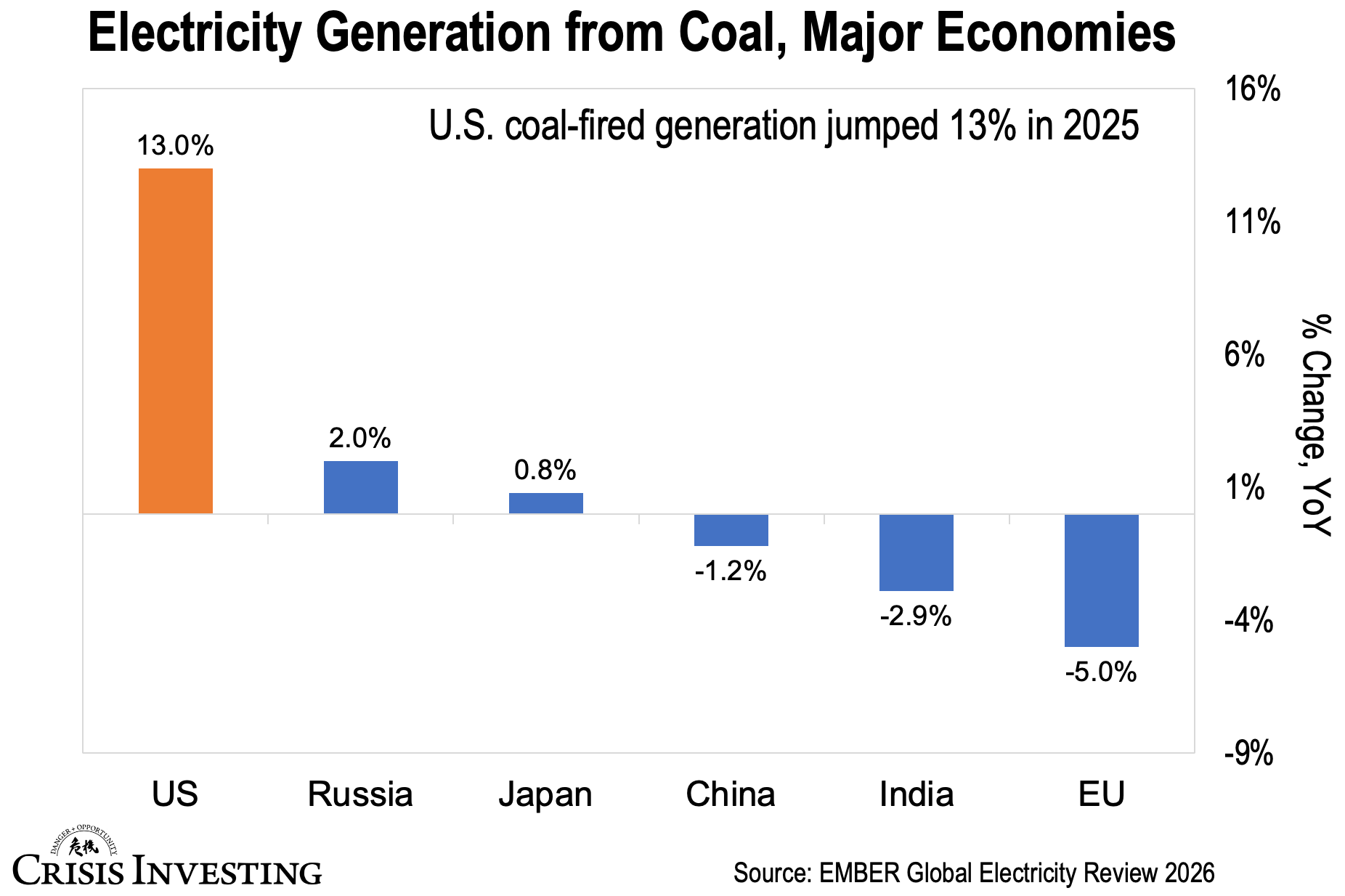

A reader recently pointed me at a chart that fits the thesis so well I had to share it. It comes from EMBER’s Global Electricity Review 2026 — the UK-based energy think tank’s annual snapshot of how the world generates electricity. This particular chart breaks out the year-over-year change in coal-fired generation in 2025 across the world’s major economies.

Take a look at the top line. The United States burned 13% more of it in 2025. It’s the single biggest year-on-year jump on the chart — more than six times the next largest gain — in the country every analyst had written off as a structural coal decliner.

Keep in mind, the U.S. had spent two decades retiring coal plants.

Now here’s the bigger story: this is 2025 data. Before Hormuz closed. Before the war with Iran. Before oil hit triple digits and the world started scrambling for energy at any price. None of that has hit this chart yet.

And look at Japan in that light. “High-tech” Japan — which imports 87% of its total energy and still gets roughly a quarter of its electricity from coal — was already burning 0.8% more of it in 2025, while LNG was still arriving on schedule. Now imagine where that number’s heading today, with Hormuz closed, two-thirds of Japan’s oil supply blocked, and emergency LNG reserves measured in weeks of cover.

Okay, but what about India and China — the apparent decliners on this graph? Well, what we do know is that both of them were already pivoting from those declines in early 2026, before the war. In 2025, China commissioned 78 gigawatts of new coal capacity — the most in a decade. Thermal-power commissioning in the first two months of 2026 alone surged over 400% to a record high. Coal-fired generation in China has now risen four months in a row. India, meanwhile, is on track for its biggest annual coal-capacity build in a decade and is forecast to post the second-largest increase in global coal consumption in 2026, up roughly 2.5% to 1.35 billion metric tons.

All of that, again, was already underway before Hormuz.

My guess is that top bar won’t still read 13% by the time next year’s review comes out. It’ll probably be a number that makes 13% look small. And the bars below — Japan, and almost certainly India and China — will flip from gentle drifts into something that finally matches what’s actually happening on the ground. As for the EU? Same direction, probably — though its leadership has been so irrationally incompetent on energy that it's genuinely hard to call.

Regards,

Lau Vegys

P.S. In our latest issue of Crisis Investing, we put forward two new picks built specifically for this coal thesis. If you’re a paid subscriber, make sure you haven’t missed it. And if you’re not yet on the paid side, the lead — featuring Doug Casey on why coal never really died — is free to all.

Startling, and I'm sure coal use is going to continue to rise. I was under the impression that coal use had risen in China as well. Thanks for the detail.

Have you looked at Frontieras? It's a startup that's way beyond the testing stage and breaking ground in coal country. They're taking coal to a whole new level.

I love their willingness to allow little guys to invest from the get-go, instead of limiting it to accredited investors.